Table of Contents >> Show >> Hide

- What Is the General Savings Benchmark for Your 30s?

- What Should Count as Savings in Your 30s?

- What Do Real Savings Numbers in Your 30s Look Like?

- How Much Should You Save Each Month in Your 30s?

- Why Your 30s Often Feel Financially Harder Than Expected

- What If You Are Behind on Savings?

- A Better Question: What Should Your Savings Strategy Look Like in Your 30s?

- The Bottom Line on How Much You Should Have Saved in Your 30s

- Experiences People Commonly Have in Their 30s With Saving Money

- SEO Tags

Your 30s are where personal finance stops being a cute little side quest and starts acting like the main plot. One day you are splitting appetizers and forgetting your gym password, and the next day you are comparing mortgage rates, daycare costs, and whether your retirement account has enough in it to keep Future You from becoming dramatically annoyed.

So, how much should you have saved in your 30s? The honest answer is: enough to make progress in several directions at once. That means retirement savings, emergency savings, and goal-based savings for the life events that love to show up in this decade uninvited but very expensive.

Still, most people want a number. A benchmark. Something more useful than “do your best” and less terrifying than “you should already be rich.” The good news is that there are practical guidelines. The better news is that these benchmarks are meant to guide you, not judge you. Your savings target depends on your income, debt, lifestyle, family situation, and whether your job feels stable or like a reality show cliffhanger.

In this guide, we will break down how much you should ideally have saved in your 30s, what counts as “saved,” what to do if you are behind, and how to build a realistic plan without giving up coffee, joy, or basic human dignity.

What Is the General Savings Benchmark for Your 30s?

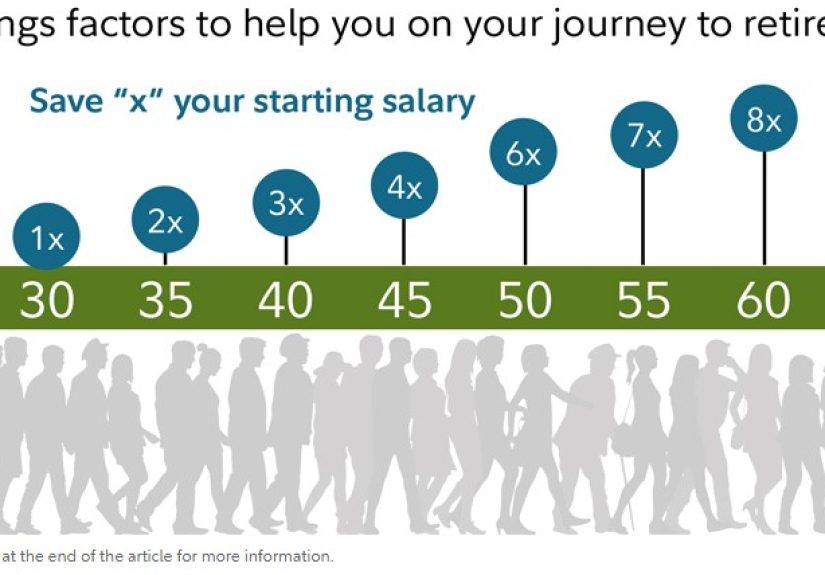

When people ask how much they should have saved in their 30s, they are usually talking about retirement savings. That is where the most widely cited benchmarks come in.

A common rule of thumb says you should aim to have about 1x your annual salary saved by age 30 and around 3x your salary saved by age 40. That means your 30s are the bridge between having a solid start and building real momentum. If you are 35, many planners would say you are doing reasonably well if you have somewhere around 1 to 1.5 times your salary saved for retirement.

Let’s make that less abstract:

- If you earn $50,000 a year, a rough target is about $50,000 saved by 30, around $50,000 to $75,000 by 35, and $150,000 by 40.

- If you earn $80,000 a year, the rough target becomes $80,000 by 30, about $80,000 to $120,000 by 35, and $240,000 by 40.

- If you earn $120,000 a year, the rough target is $120,000 by 30, around $120,000 to $180,000 by 35, and $360,000 by 40.

These numbers are not magical. They are planning markers. They assume you are saving steadily over time, often around 15% of income including employer contributions. They also assume you want to maintain a similar lifestyle in retirement, not retire to a treehouse with two shirts and a suspicious amount of optimism.

What Should Count as Savings in Your 30s?

This is where people accidentally confuse themselves. If you have money in five places, a car loan, and a random savings app you forgot existed, your financial life can feel like a scavenger hunt.

Retirement Savings

Your 401(k), 403(b), IRA, Roth IRA, and similar long-term investment accounts usually make up the core of your “how much should I have saved” number. These accounts are designed for retirement, often come with tax advantages, and in the case of employer plans may include matching contributions. If your company offers a match and you are not taking it, that is basically the financial equivalent of leaving fries on the table.

Emergency Savings

You also need liquid cash. Not invested. Not tied up in a retirement account. Not hidden in a drawer labeled “travel fund” when it is actually your “car battery exploded” fund. An emergency fund should cover unexpected costs like medical bills, job loss, urgent repairs, or surprise travel. In your 30s, a practical target is often three to six months of essential expenses, though some people need more depending on job stability, family size, and debt obligations.

Goal-Based Savings

Your 30s often come with medium-term goals that do not fit neatly into retirement planning. That might include a down payment, moving costs, fertility treatment, weddings, grad school, a new business, or replacing the car that has started making sounds like a haunted washing machine. Money for these goals matters too, but it should usually be tracked separately from retirement savings so you know what is actually doing what.

What Do Real Savings Numbers in Your 30s Look Like?

Benchmarks are useful, but real-life balances tell a humbling story. Median retirement balances for Americans in defined-contribution plans are much lower than the glossy benchmark charts. That does not mean the benchmarks are fake. It means many people are behind, often because life is expensive, debt is real, and your 30s are financially crowded.

In workplace retirement plans, the median balance for people ages 25 to 34 is far below the “1x salary by 30” dream, and the median for ages 35 to 44 is still much lower than what many benchmark models suggest. That gap exists because benchmarks are aspirational targets, while median balances reflect real households juggling rent, student loans, childcare, inflation, and a thousand other budget-eating goblins.

So if you are in your 30s and feel behind, you are not weird. You are normal. The goal is not to win the comparison Olympics. The goal is to improve your trajectory.

How Much Should You Save Each Month in Your 30s?

A good long-term target is to save about 15% of your gross income for retirement, especially if you are aiming for a traditional retirement timeline. If that sounds impossible right now, start with the employer match, then increase your savings rate by 1% every few months or every time you get a raise.

Here is a simple framework that works well in your 30s:

- First: Contribute enough to get the full employer match.

- Second: Build or maintain an emergency fund.

- Third: Increase retirement contributions toward 15%.

- Fourth: Save separately for medium-term goals like a home, children, or business plans.

- Fifth: Pay down high-interest debt aggressively.

If you have access to tax-advantaged accounts, use them. In 2026, the employee contribution limit for many workplace retirement plans is $24,500, and the IRA limit is $7,500. Most people in their 30s will not max these out, and that is fine. The real win is using the accounts consistently and increasing contributions over time.

Why Your 30s Often Feel Financially Harder Than Expected

There is a reason this decade feels expensive. Your income may be higher than it was in your 20s, but your obligations are usually bigger too. Housing costs rise. Weddings happen. Babies happen. Home repairs happen. Dental work appears from nowhere like a villain with excellent timing.

Spending data shows American households are dealing with large annual expenses, and core categories like housing eat an enormous share of the budget. In plain English: even decent earners can feel cash-strapped. That is exactly why savings goals in your 30s should be realistic, flexible, and automated wherever possible.

What If You Are Behind on Savings?

Then welcome to the club. It has millions of members, and nobody got a tote bag.

Being behind does not mean you are doomed. It means you need a plan that is sharper than “I should probably save more.” Here is what actually helps.

1. Stop Using One Giant Number as Your Only Scorecard

Do not obsess over whether you have exactly one salary saved by 30 or exactly three by 40. Instead, ask better questions: Am I saving consistently? Am I capturing my employer match? Is my emergency fund growing? Is my debt load shrinking? Am I improving year over year?

2. Automate the Process

Automatic payroll contributions, automatic transfers to savings, and automatic annual increases take emotion out of the equation. This matters because discipline is helpful, but systems are better. Systems still work on the days when you are tired, distracted, or one click away from buying patio furniture you absolutely do not need.

3. Increase Your Savings Rate Gradually

If jumping from 4% to 15% makes your budget cry, go from 4% to 6%, then to 8%, then higher over time. Small increases are powerful because they are sustainable.

4. Attack High-Interest Debt

Credit card debt charging double-digit interest can wreck your ability to build wealth. If you have an employer match, grab it first. After that, it may make sense to direct extra cash toward high-interest debt while still saving enough to keep momentum alive.

5. Protect Your Cash Buffer

If you do not have an emergency fund yet, build a starter one fast. Even a modest buffer can prevent you from raiding retirement accounts or leaning on credit cards when life gets messy. And life, as your 30s will cheerfully demonstrate, does get messy.

A Better Question: What Should Your Savings Strategy Look Like in Your 30s?

The best strategy is not just “save more.” It is to save with purpose.

If You Are 30 to 33

Focus on establishing the habit. Get the full employer match, automate contributions, and build a starter emergency fund. If your income is still growing, your biggest financial superpower is consistency plus time.

If You Are 34 to 36

This is a great time to check whether your retirement balance is roughly in the neighborhood of one to one-and-a-half times your salary. If not, increase contributions, cut one or two recurring expenses that truly do not matter, and direct raises toward savings instead of lifestyle inflation.

If You Are 37 to 39

Now the runway to 40 starts to matter more. Review your progress, rebalance your investment mix if needed, and make sure you are saving not only for retirement but also for predictable major costs. By this point, “I’ll deal with it later” becomes a very expensive financial strategy.

The Bottom Line on How Much You Should Have Saved in Your 30s

A strong rule of thumb is this: aim for about 1x your salary by 30, around 1 to 1.5x by 35, and close to 3x by 40. Alongside that, build an emergency fund that can cover several months of essential expenses and keep saving for near-term goals separately.

But do not confuse a benchmark with a verdict. If you are not there yet, that does not mean you failed. It means you have information. And information is useful. You can adjust your savings rate, automate your plan, lower expensive debt, and steadily improve your position.

Your 30s are not the decade where you must have everything perfectly figured out. They are the decade where your financial habits start compounding into something powerful. Start where you are. Use the numbers as guideposts. Keep moving. Future You may not send a thank-you card, but they will probably sleep better.

Experiences People Commonly Have in Their 30s With Saving Money

One of the strangest things about saving in your 30s is that your income can go up while your feeling of financial comfort does not. A lot of people enter this decade assuming that once they earn more, money stress will fade. Then real life shows up wearing expensive shoes. Rent or mortgage payments increase. Insurance costs rise. Someone needs braces. Someone else needs a new transmission. Suddenly you are making more money than you did at 26 but somehow feeling less relaxed.

Another common experience is the emotional whiplash of comparison. In your 30s, your friends stop being financially similar to you. One friend is buying a house. Another is moving back in with family to pay off debt. One is maxing out retirement accounts. Another is trying to rebuild after a layoff or divorce. If you compare your savings to the loudest success story in your social circle, you will probably feel behind. If you compare your current self to your past habits, you will get a much more useful picture.

Many people also discover that saving gets easier once it becomes boring. In your 20s, finance often feels dramatic: new job, first apartment, first real salary, first investment account. In your 30s, the biggest wins usually come from extremely unglamorous behavior. Automatic transfers. Payroll deductions. Repeating the same good decisions every month. It is not thrilling, but it works. Wealth building often looks less like a movie montage and more like setting up transfers and then going outside.

There is also the experience of having multiple savings goals compete with each other. You may want to save for retirement, but also for a home, a wedding, a baby, a business idea, a move, or a sabbatical. That tension is normal. It does not mean you are bad at money. It means you are living a full adult life. The trick is giving each goal a job. Retirement money should be for retirement. Emergency savings should be for emergencies. House savings should not quietly become vacation savings because airline prices made you feel spontaneous.

For a lot of people, their 30s are also when one financial lesson finally lands: stability has value. Having cash in savings may not feel as exciting as chasing investment returns, but it creates breathing room. It lets you handle a rough month without panic. It gives you options if a job becomes unbearable. It helps you make decisions from a position of strength instead of desperation. That feeling of “I can handle this” is one of the most underrated benefits of saving money.

And finally, many savers in their 30s learn that progress rarely looks dramatic in real time. It looks like paying yourself first. It looks like increasing your contribution rate by 1%. It looks like saying no to one unnecessary subscription and yes to one automatic transfer. Then one day you check your balances and realize you are no longer improvising. You are building something. Maybe not perfectly. Maybe not as fast as you hoped. But steadily, intentionally, and with far fewer money-related panic spirals than before. That is real progress, and in your 30s, real progress counts for a lot.