Table of Contents >> Show >> Hide

- The Short Answer: Yes, Prices Can Fall, but Not Every Recession Creates a Housing Crash

- Why the Housing Market Looks Vulnerable Right Now

- Why the Next Recession Might Not Crush Home Prices Nationwide

- What Usually Determines Whether Prices Fall a Little or a Lot

- What the Most Likely Scenario Looks Like

- What Buyers Should Do if They Expect a Recession

- What Sellers Should Do if They Fear a Downturn

- The Bottom Line

- Real-World Experiences Related to “Will Housing Prices Fall During the Next Recession?”

Note: This article discusses the national housing market. Real estate is intensely local, so your city, neighborhood, and price range may behave very differently from the national average.

When people start whispering the word recession, the housing market instantly becomes the main character in everyone’s group chat. Buyers wonder whether they should wait for lower prices. Sellers wonder whether they should list now before the floor drops out. Homeowners with a 3% mortgage rate clutch their monthly payment like it is a family heirloom. And investors start acting like every spreadsheet cell contains a prophecy.

So, will housing prices fall during the next recession? The honest answer is: probably in some places, maybe modestly at the national level, but a dramatic nationwide crash is far from guaranteed. Recessions do not automatically produce a housing collapse. Home prices usually respond to a mix of job losses, mortgage rates, inventory levels, lending standards, and seller behavior. In other words, the housing market is not a vending machine where you press “recession” and out pops a 25% discount.

Today’s market is especially tricky because the ingredients are mixed. Affordability is still stretched, mortgage rates remain elevated compared with the pandemic era, and homes are taking longer to sell. At the same time, inventory is still relatively tight by historical standards, credit quality is much stronger than it was before the 2008 crash, and many homeowners are sitting on low-rate mortgages with no desire to move unless life absolutely drags them into it.

That combination matters. It suggests that the next recession, if one arrives, is more likely to produce a slow, uneven, local correction than a massive coast-to-coast home-price collapse. Some overheated metros could see meaningful declines. Other markets might simply flatten out, offer more negotiation room, or post mild price dips that feel bigger emotionally than they look on paper. A seller who has to cut $20,000 from a list price will definitely feel it. A historian looking back at the chart may call it “modest softening.” Both people can be annoyingly correct at the same time.

The Short Answer: Yes, Prices Can Fall, but Not Every Recession Creates a Housing Crash

Housing prices can absolutely fall during a recession. Demand often weakens when consumers worry about layoffs, income growth slows, and lenders become more cautious. Buyers pull back. Sellers get nervous. Homes sit longer. Negotiation returns from vacation. All of that can push prices lower.

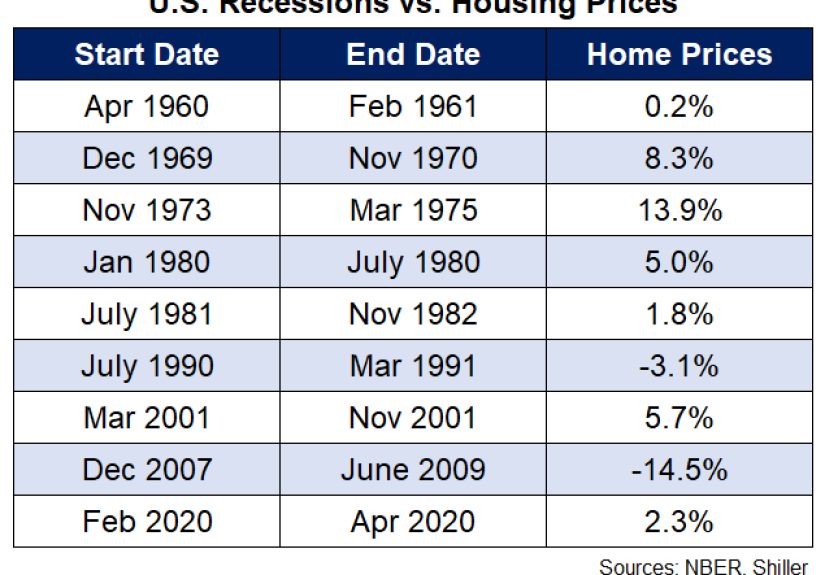

But the key mistake is assuming that every recession looks like 2008. The Great Recession was not just a normal economic downturn. It was a housing and credit crisis wrapped in a financial crisis, wearing a recession as an accessory. That is why prices fell so severely in that period. The combination of loose lending, speculative buying, overbuilding in many areas, rising foreclosures, and highly leveraged financial institutions turned housing weakness into a national wrecking ball.

That setup is not the default setting today. Lending standards have been tighter for years. Vacancy rates remain low. There is no broad sign of speculative overbuilding on the scale that defined the mid-2000s bubble. Many current owners also have sizable equity cushions, which lowers the odds of a forced-selling wave unless unemployment jumps sharply and stays high for longer than expected.

That does not mean prices are bulletproof. It means the path to lower prices now is different. Instead of a foreclosure tsunami, the next downturn would more likely hit through affordability strain, hesitant buyers, longer time on market, more price cuts, and selective local oversupply. That is a much slower, more uneven mechanism.

Why the Housing Market Looks Vulnerable Right Now

1. Affordability is still rough for ordinary buyers

Even with some improvement in affordability over the past year, homeownership remains expensive. Mortgage rates are still elevated compared with the ultra-low era many buyers remember with suspicious nostalgia. Monthly payments, property taxes, insurance costs, maintenance, and higher down payment requirements have kept many households on the sidelines. When housing is expensive before a recession starts, demand is already fragile. It does not take a huge shock to make buyers pause.

This is especially true for first-time buyers, who do not have home equity from a previous sale to cushion the blow. A mild recession can lead this group to wait longer, shop lower, or disappear from the market entirely. When entry-level demand weakens, the softness can ripple upward because move-up sellers depend on first-time buyers entering the chain.

2. Homes are taking longer to sell

One of the earliest signs of cooling is not always falling prices. Sometimes it is simply time. Homes stay on the market longer. Sellers get fewer offers. Open houses become less like a concert and more like a quiet museum exhibit where two people show up and one is just there for decorating ideas.

That slower pace matters because prices tend to soften after market velocity weakens. First comes longer marketing time. Then come concessions, credits, repairs, and price reductions. Then, if the slowdown lasts, closed-sale prices begin to reflect the softer conditions more clearly.

3. Inventory is rising, even if it is not fully back to normal

Inventory has improved from the extreme shortage years, and that is good news for buyers. More homes on the market means more options, more comparison shopping, and less desperation. But the story is not simple. Inventory may be rising relative to the recent past while still sitting below pre-pandemic norms in many areas. That means supply is better, but not necessarily abundant.

This distinction is crucial. A recession paired with normal or tight inventory may only flatten prices. A recession paired with a fast inventory build can produce sharper declines, especially in markets where sellers have to compete aggressively.

4. Some local markets already look softer than others

National headlines flatten reality. Underneath them, local markets are doing very different things. Some Midwest metros have shown stronger price growth, while several expensive or pandemic-boom markets have already posted price declines or weaker demand. That split is a warning sign for anyone expecting one neat national answer.

If the next recession arrives, price declines are likely to cluster where affordability is worst, investor demand has cooled, construction added supply faster, or in-migration has slowed. Areas that never got too frothy, or still suffer from chronic supply shortages, may hold up much better.

Why the Next Recession Might Not Crush Home Prices Nationwide

1. Many homeowners are locked into low mortgage rates

The so-called lock-in effect remains powerful. Millions of homeowners refinanced or bought when rates were much lower. Selling now often means giving up a comfortable mortgage payment and replacing it with a much uglier one. That reduces supply because many owners simply choose not to move.

In a recession, this behavior can act like a shock absorber. Normally, weaker demand would be met with a flood of anxious sellers. But if owners are financially comfortable and unwilling to trade their low rate for a higher one, supply may stay tighter than expected. Less forced selling usually means less downward pressure on prices.

2. Homeowners have more equity than in the last big crash

Equity matters because it changes how people behave under stress. An owner with a strong equity cushion has more options: sell conventionally, rent the property, negotiate, or simply wait. An owner who is underwater has far fewer choices and may become distressed more quickly. The current market has more built-in equity support than the mid-2000s bubble did, which reduces the odds of a broad foreclosure-driven collapse.

3. Lending standards have been tighter

Loose credit helped inflate the bubble before the financial crisis. Today’s mortgage market is much more conservative. That does not eliminate risk, but it does reduce the likelihood of a giant chain reaction where weak loans, falling prices, and financial instability feed on one another. Fewer reckless loans usually means fewer catastrophic defaults when the economy slows.

4. Supply is still structurally constrained in many regions

The United States still faces a long-running housing supply problem in many markets. Zoning constraints, high land costs, expensive construction, labor shortages, and insurance pressures all limit how fast supply can grow. A recession can reduce demand, but if supply remains restricted, price declines may be smaller than many buyers hope.

That is why a national recession does not automatically translate into a national bargain bin. A weak economy may cool bidding wars without producing dramatic markdowns. Buyers may gain negotiating power, but not necessarily dream-home-at-2019-prices power.

What Usually Determines Whether Prices Fall a Little or a Lot

Unemployment

Job losses are one of the biggest swing factors. If a recession is mild and employment remains relatively resilient, homeowners are less likely to sell under pressure. If unemployment climbs quickly and stays high, distress rises, demand weakens, and prices face more serious pressure.

Mortgage rates

Mortgage rates can offset part of recession damage if they decline enough to revive demand. Lower rates improve affordability, increase buying power, and can put a floor under prices. But the relationship is not automatic. If fear is widespread and layoffs are rising, buyers may still hesitate even if rates improve. A cheaper mortgage does not feel very comforting when someone is worried about keeping their paycheck.

Inventory growth

The speed of inventory growth matters as much as the raw number. If listings rise faster than buyers return, sellers start competing on price and concessions. If inventory only inches up, the market may remain more balanced than bearish.

Local supply pipelines

New construction can either cushion or worsen price weakness. In markets where builders already have a lot of inventory, they may offer rate buydowns, discounts, upgrades, and closing-cost help. That can pressure resale sellers nearby. In markets where construction remains limited, builders may not have enough supply to create a real pricing reset.

Household finances

Consumer balance sheets, savings, debt burdens, and payment stress all matter. A recession hits harder when households are already stretched thin. If owners remain relatively stable, they can stay put, and the market avoids a panic cycle.

What the Most Likely Scenario Looks Like

The most likely national scenario is not a crash. It is a patchwork market.

In that scenario, national home prices might post flat growth, a mild decline, or only small year-over-year moves, while individual metros show much larger swings. Expensive Sun Belt and West Coast markets with affordability pressure or softer migration trends may see deeper cuts. More affordable Midwest or Northeast markets with tighter supply may prove more resilient. Sellers in some areas will need to price realistically from day one. Sellers in other areas will still attract competition if they offer the right home at the right price.

That uneven outcome is exactly what makes broad forecasts so frustrating. The answer to “Will housing prices fall?” may be “yes” in one zip code, “not much” in another, and “actually still rising” somewhere else. Real estate loves making economists sound too confident and homeowners sound too dramatic. It is one of its core hobbies.

What Buyers Should Do if They Expect a Recession

Focus on payment, not fantasy

Waiting for a giant national price collapse may leave buyers stuck on the sidelines indefinitely. A smarter move is to focus on the monthly payment, job stability, emergency savings, and how long you plan to stay in the home. If the payment is safe and the property fits your life for several years, a modest future price swing matters less.

Shop for leverage, not just price cuts

In a softer market, savings may appear through seller credits, repair concessions, rate buydowns, and better contract terms rather than dramatic list-price drops. A buyer who only watches the sticker price may miss the real deal.

Know your local market

National data is useful, but local months of supply, job growth, new construction, and days on market matter more for an actual purchase. If your market is still inventory-starved, waiting for a huge discount could become an expensive hobby.

What Sellers Should Do if They Fear a Downturn

Price ahead of the market, not behind it

In a slowing market, yesterday’s comparable sale can become a dangerous comfort blanket. Sellers who overprice often end up chasing the market down. The best strategy is usually to price realistically at the start, create urgency, and avoid a long stale listing that invites lowball offers.

Expect negotiation to return

The era of “as-is, waive everything, write a love letter to the laundry room” is not the permanent law of real estate. In a weaker market, buyers ask for repairs, credits, and time. Sellers who accept this reality early generally do better than those who treat every request as a personal attack.

Understand your real competition

Your competition is not just the house next door. It is also the new-build community offering incentives, the renovated listing down the street, and the homeowner who already cut the price twice. Strategy matters more than pride.

The Bottom Line

Will housing prices fall during the next recession? Some probably will. But that does not automatically mean a dramatic nationwide collapse. The current housing market has real pressure points: affordability is stretched, demand is sensitive, and more listings are giving buyers extra room to negotiate. At the same time, today’s market still has important supports, including tighter lending standards, stronger homeowner equity, low vacancy, and the lock-in effect keeping many owners from flooding the market.

The most realistic expectation is a slower, more selective adjustment. A mild recession could bring flatter prices, more regional declines, and better negotiating conditions without causing a replay of the housing crash. A deeper recession with sharp job losses could push the correction further. Either way, local conditions will matter far more than national panic headlines.

If you are buying, selling, or simply stress-refreshing mortgage-rate charts, the smartest approach is to think in probabilities, not absolutes. Housing is rarely all boom or all bust. More often, it is a messy middle filled with compromises, spreadsheets, and at least one relative insisting prices will be “back to normal by summer.”

Real-World Experiences Related to “Will Housing Prices Fall During the Next Recession?”

In real life, people do not experience recessions through charts. They experience them through awkward listing appointments, second thoughts in the lender’s office, and late-night calculator sessions at the kitchen table. That is why the emotional side of housing matters almost as much as the economic side.

For many first-time buyers, recession fear creates a strange mix of hope and anxiety. They hope prices will soften enough to open the door to ownership, but they also worry that job cuts, tighter lending, or sudden rate volatility could make the purchase riskier. A lot of buyers in this position do not necessarily stop shopping. Instead, they become more selective. They compare neighborhoods more carefully, insist on inspections, negotiate harder, and refuse to stretch their budgets just to “win” a house. Their experience is less about chasing the lowest possible price and more about avoiding a costly mistake.

Current homeowners often experience the topic differently. Owners with ultra-low mortgage rates tend to feel trapped and protected at the same time. They may want to move for family, work, school, or lifestyle reasons, but the idea of swapping a cheap mortgage for a much higher payment can make them freeze. Even if they believe home prices could soften in a recession, many still choose to stay put because the replacement home looks too expensive. That hesitation can reduce supply and help support prices, which is one reason the market can remain stubborn even when confidence weakens.

Sellers going into a downturn usually learn one big lesson quickly: buyers become much less forgiving. In a hot market, a dated kitchen, a worn roof, or an overambitious list price might still attract traffic. In a softer market, those flaws suddenly become bargaining chips. Sellers who adapt early often say the same thing afterward: the market did not punish them for selling, but it did punish them for ignoring reality. Flexible sellers usually preserve more value than stubborn sellers who spend months chasing the market lower.

Investors and second-home buyers often have yet another experience. They tend to react faster to changing conditions because they are less emotionally tied to the property. If rents soften, insurance rises, or appreciation slows, they may pull back quickly. In some markets, that retreat removes an important source of demand and adds more downward pressure on prices. In others, long-term investors step in when owner-occupants get nervous, which helps stabilize the market.

The clearest takeaway from real-world experience is that housing during a recession is rarely one dramatic event. It is usually a series of smaller decisions: who can wait, who must move, who can negotiate, and who gets priced out. That is why the answer to this question is never just about whether prices fall. It is also about how people behave when uncertainty shows up at the front door.