Table of Contents >> Show >> Hide

- Why People Keep Writing Active Management’s Obituary

- The Hard Truth: Active U.S. Stock Picking Usually Struggles

- So Why Is Active Management Still Alive?

- The Rise of Active ETFs Changed the Conversation

- Where Active Management Can Still Earn Its Keep

- Where Passive Usually Wins

- What Investors Should Ask Before Choosing Active Management

- Conclusion: Alive, but on a Shorter Leash

- Extended Experiences and Real-World Lessons About Active Management

- SEO Tags

Active management has been declared dead so many times that it deserves its own zombie franchise. Every few years, someone points at index fund flows, low-cost ETFs, and another grim performance scorecard and says, “Well, that settles it.” Then active managers show up again, adjusting bond portfolios, launching new ETFs, hunting mispriced securities, and generally refusing to stay buried. So the better question is not whether active management is dead. It is whether active management still earns its keep.

The honest answer is more interesting than the usual “active bad, passive good” bumper sticker. In much of U.S. stock investing, active management has had a rough time. Costs are higher, taxes can be messier, and many managers fail to beat their benchmarks over long stretches. But that is not the whole story. Active management still matters in less efficient corners of the market, especially fixed income, specialized mandates, downside-conscious strategies, and the increasingly popular world of active ETFs.

In other words, active management is not dead. It has just lost the luxury of being taken for granted.

Why People Keep Writing Active Management’s Obituary

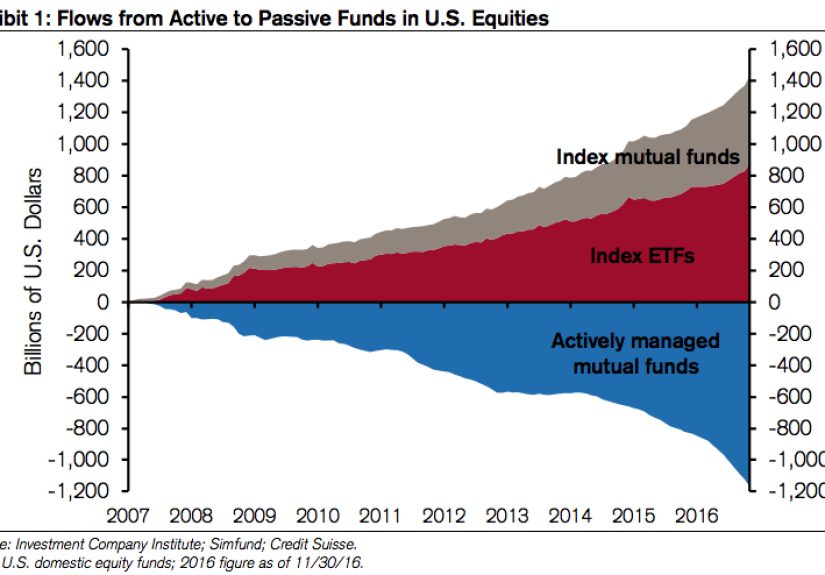

The case against active management is not hard to understand. Index investing has become the default choice for millions of Americans because it is simple, cheap, diversified, and brutally difficult to beat over time. When a passive fund tracks a broad benchmark like the S&P 500, the pitch is wonderfully boring: own the market, keep fees low, stay patient, and let compounding do the heavy lifting.

That approach gained momentum for a reason. Scorecards that compare active funds with their benchmarks keep reminding investors that many active equity managers do not outperform after fees. In large-cap U.S. equities, that pattern has been especially stubborn. When mega-cap stocks dominate returns and markets become harder to outguess, stock pickers can start looking like people trying to win a Formula 1 race on roller skates.

Costs also matter more than many investors realize. An active manager does not get a free pass simply for being smart, experienced, or excellent on CNBC. To justify higher fees, higher turnover, research costs, and trading decisions, the manager has to generate enough excess return to overcome all of that friction. That is a tall order, and the longer the time horizon, the harder it becomes.

Then there is survivorship. Investors often remember the winners because winners get interviews, assets, and flattering profile pieces. The losers get merged away, shut down, or quietly escorted out the side door. That makes active management look better in casual conversation than it often looks in full-universe studies.

The Hard Truth: Active U.S. Stock Picking Usually Struggles

If you want the uncomfortable truth in plain English, here it is: on average, active U.S. equity managers have not made a convincing long-term case against broad passive exposure. Large-cap U.S. stocks are heavily researched, highly liquid, and widely owned. That means it is difficult to discover persistent informational advantages. Everyone is looking at the same earnings calls, the same economic data, and the same market-moving headlines.

When active managers lag, it is usually not because they are foolish. It is because they are competing in one of the toughest arenas in finance. A talented manager can still outperform in a given year. A handful may outperform over longer periods. But the average investor is not shopping for “a handful.” The average investor is choosing from a crowded shelf filled with products, narratives, marketing, and fees.

That is why passive investing keeps winning the popularity contest. It asks less from the investor. You do not need to identify the next star manager, guess whether a hot streak is skill or luck, or wait three years hoping a “disciplined process” eventually begins paying rent.

For taxable investors, the passive argument often gets even stronger. Lower turnover can mean fewer capital gains distributions and less surprise tax drag. That may not sound exciting, but boring tax efficiency is one of those gifts that gets better with age.

So Why Is Active Management Still Alive?

Because markets are not all built the same.

Even critics of active equity management usually acknowledge that some areas are more favorable to skilled managers than others. Fixed income is the clearest example. Bond markets are enormous, fragmented, and often less transparent than stock markets. Securities do not all trade with the same frequency. Index construction can create strange incentives. Credit quality, maturity, duration, liquidity, call features, and issuer fundamentals all matter. Suddenly, the manager is not just choosing between Company A and Company B. The manager is navigating a maze.

That complexity creates room for judgment. An active bond manager may tilt duration, avoid weaker issuers, exploit relative value, manage credit exposure, or seek better liquidity. In other words, active management in bonds is not just about “beating the index” in a simple stock-picking sense. It can also be about risk control, income management, and avoiding the ugliest potholes in the road.

Active management may also matter in narrower equity categories, niche markets, or capacity-constrained strategies where the benchmark does not perfectly represent opportunity. Small-cap stocks, less-covered international names, event-driven situations, or strategies with downside discipline can sometimes offer more room for skill than a plain-vanilla U.S. large-cap blend fund.

And then there is product evolution. Active mutual funds may have lost some glamour, but active ETFs have become one of the liveliest corners of the asset management business. Investors like ETFs for liquidity, transparency, convenience, and, in many cases, better tax efficiency. Managers like them because the ETF wrapper gives active strategies a fresher, more flexible way to compete in a market that increasingly punishes expensive, sleepy legacy products.

The Rise of Active ETFs Changed the Conversation

This is one of the strongest arguments against the “active management is dead” narrative. A dead business usually does not reinvent itself this quickly.

Active ETFs have grown rapidly because they speak both languages: the investor’s demand for modern, low-friction vehicles and the manager’s desire to apply research, security selection, and risk management. They are not automatically cheap, and they are not automatically better, but they show that investors have not rejected active management entirely. They have simply become less willing to tolerate old-fashioned pricing and vague promises.

That shift matters. Investors are saying, “If you want my money, bring a clear edge, price it competitively, and put it in a structure I actually like.” That is not a funeral. That is a performance review.

Some firms have responded well. Instead of insisting that every investor needs fully active stock picking everywhere, they now offer blended solutions: passive core holdings, active satellite positions, active bond sleeves, tactical income strategies, or factor-aware portfolios. The result is a more realistic investment landscape where active management does not have to dominate the whole portfolio to earn a place in it.

Where Active Management Can Still Earn Its Keep

1. Bonds and fixed income

This is the strongest case. Bond markets are less standardized than stock markets, and active managers can potentially add value through credit selection, duration management, liquidity analysis, and risk control. For investors who care about income and downside management, active bond funds can still be useful tools.

2. Specialized or inefficient market segments

Active management has a better chance when the market is less efficient, less liquid, or less thoroughly researched. The farther you move from the most heavily analyzed large-cap U.S. names, the better the odds that skill can matter.

3. Risk-managed mandates

Some investors are not trying to beat the market in every calendar year. They may want smoother returns, lower drawdowns, income stability, or more defensive positioning. In these cases, success should be measured against the investor’s objective, not just a headline benchmark.

4. Active ETFs with sensible fees

Active ETFs are not a magic wand, but they can narrow the gap between what investors want and what active managers offer. Lower friction, daily tradability, and a more modern structure make them easier to justify than some older products with high expense ratios and little differentiation.

Where Passive Usually Wins

Passive investing remains the default winner in several situations. It usually makes the most sense for broad U.S. large-cap equity exposure, long-term retirement savings, fee-sensitive investors, beginners who want simplicity, and anyone who does not want to spend time evaluating managers. It also works well as a portfolio’s foundation, even when active strategies are added around the edges.

That last point matters. The active-versus-passive debate is often framed like a cage match, but most investors do not need to pick one ideology and tattoo it on their forehead. A low-cost passive core with selective active exposure can be perfectly rational. In fact, it is often more rational than adopting an all-or-nothing identity.

What Investors Should Ask Before Choosing Active Management

If active management is going to live in your portfolio, it should answer a few uncomfortable questions first.

What is the manager’s actual edge? “We do deep research” is not an edge. Everyone says that. Look for a clear explanation of where the strategy expects to add value and why that opportunity should persist.

Is the fee reasonable? Fees are not a side note. They are part of performance. A manager who charges premium prices for average results is not sophisticated. That is just expensive disappointment in a blazer.

What role does the strategy play? Is it meant to generate alpha, reduce volatility, improve income, manage risk, or complement passive holdings? A strategy without a clear job description tends to wander.

How does it behave in different environments? Good investing is not about looking brilliant in one lucky year. It is about understanding how a strategy behaves when markets are euphoric, fearful, concentrated, or flat-out weird.

Would I still hold this after a bad year? This is the question investors hate because it requires honesty. Active strategies can underperform for long stretches. If you are likely to bail at the worst possible time, a passive option may be better for your actual behavior, not just your spreadsheet self.

Conclusion: Alive, but on a Shorter Leash

So, is active management still alive? Absolutely. Is it thriving everywhere? Not even close.

In broad U.S. equities, passive investing has earned its dominance by being low-cost, efficient, and hard to beat. Active stock pickers still face a steep uphill climb, and investors should be skeptical by default. But skepticism is not the same thing as a eulogy. Active management continues to matter in bonds, specialized niches, risk-managed strategies, and the rapidly expanding active ETF market.

The real story is not that active management died. It is that the easy version died. The era when active managers could charge more, explain less, and expect loyalty just because they looked busy is fading. Today, active management has to be sharper, cheaper, clearer, and more accountable.

That is probably good news for investors. When an industry has to prove it deserves to exist, the survivors usually get better.

Extended Experiences and Real-World Lessons About Active Management

One of the most common investor experiences with active management is emotional rather than mathematical. A person buys an active fund because the recent returns look terrific, the manager sounds brilliant, and the marketing story makes perfect sense. Then a year or two passes, performance cools off, and the investor starts wondering whether the strategy was ever special at all. This cycle is so common that it deserves its own warning label: “May cause overconfidence during good years and existential dread during normal ones.”

Another real-world pattern appears in retirement accounts. Many investors begin with a few actively managed mutual funds because that is what was available in their workplace plan or what an advisor recommended years ago. Over time, they compare fees, notice that their plain index option keeps doing just fine, and begin shifting the core of the portfolio toward passive funds. Yet they often keep one or two active positions in areas where they still believe judgment matters, such as bonds, dividend income, or international exposure. That blended approach is not glamorous, but it is very common because it matches how people actually make decisions.

Advisors see another version of this experience. Clients often say they want outperformance, but what they really want is reassurance. They want to know that someone is watching the market, adjusting risk, and trying to avoid disaster. That desire helps explain why active management remains appealing even when passive performance looks strong. For many investors, paying for judgment feels emotionally valuable, especially during stressful markets. Whether that judgment adds enough measurable value is a separate question, but the demand is real.

Bond investors frequently report a different experience altogether. They may not expect a bond manager to produce flashy returns. Instead, they care about steadier income, credit quality, duration decisions, and avoiding ugly surprises when rates move or defaults rise. In that context, active management can feel more intuitive. The investor is not asking for heroic stock-picking magic. They are asking for careful navigation through a market that is more complicated than many broad bond indexes suggest.

There is also a generational experience at work. Older investors often remember a time when active mutual funds dominated the menu and indexing felt like a niche philosophy. Younger investors, by contrast, often enter the market hearing that low-cost index funds are the default smart choice. That means active management now has to introduce itself to new investors from a position of skepticism rather than authority. It no longer gets automatic respect. It has to audition.

Perhaps the most useful lesson from real investor experience is this: success depends less on choosing a team in the active-versus-passive culture war and more on choosing a process you can stick with. Investors who jump from one hot active fund to another often end up disappointed. Investors who use passive funds for their core exposure and add active strategies only when they understand the role tend to make calmer decisions. The winning experience usually comes from clarity, discipline, and cost awareness, not from trying to sound like you swallowed a hedge fund glossary.

That may be the simplest answer to the title of this article. Yes, active management is still alive. But today it survives best when it solves a real problem, charges a fair price, and remembers that investors are not buying drama. They are buying outcomes.