Table of Contents >> Show >> Hide

- What “Bedrock” Really Means (And Why You Need It)

- Start With a Policy: The Portfolio’s “Constitution”

- Asset Allocation: The Biggest Lever You Control

- Diversification: Don’t Just Own More ThingsOwn Different Things

- Risk Management: The Adult Supervision Your Portfolio Deserves

- Rebalancing: The Portfolio’s Alignment Check (Not a Punishment)

- Costs and Friction: The Silent Returns Thieves

- Measurement: The Feedback Loop That Keeps You Honest

- Governance: Who Decides, Using What Rules, With What Data?

- A Practical Blueprint: Build a Portfolio That Can Survive Reality

- of Real-World Experience (The Stuff People Learn the Hard Way)

- Conclusion: The Bedrock Is Boring on Purpose

Portfolio management has a funny reputation. Some people think it’s a glamorous sport involving high-stakes predictions,

expensive coffee, and charts that look like modern art. In reality, great portfolio management is much less “fortune teller”

and much more “civil engineer.” It’s not about guessing the next hot thingit’s about building something that can stand up

to weather, time, and the occasional emotional hurricane.

That’s where the “bedrock” comes in. The bedrock of portfolio management is the set of principles and processes that stay

true even when the headlines change, the market mood swings, or your organization suddenly decides it has “strategic priorities”

(plural) that somehow all mean “do more with less.”

And here’s the twist: whether you’re managing an investment portfolio (stocks, bonds, funds) or an enterprise

portfolio (projects, products, initiatives), the bedrock looks surprisingly similar. You need clear objectives, explicit constraints,

governance that can say “no,” disciplined allocation, ongoing risk management, and a feedback loop that keeps reality from drifting

into wishful thinking.

What “Bedrock” Really Means (And Why You Need It)

Bedrock is the stuff you build on when you don’t want your house to slide down a hill. In portfolio management, bedrock is what

prevents you from “accidentally” turning a thoughtful plan into a collection of random bets, legacy baggage, and vibes.

A strong foundation does three things:

- Defines success (so you can measure it instead of arguing about it).

- Controls risk (so your portfolio doesn’t become a stress hobby).

- Creates repeatable decisions (so you don’t reinvent the wheel every quarterbadly).

Without bedrock, portfolios drift. Investments drift toward whatever has been winning lately. Project portfolios drift toward

whoever shouts the loudest. Neither is a strategy; both are a recipe for regret.

Start With a Policy: The Portfolio’s “Constitution”

For investment portfolios: the Investment Policy Statement (IPS)

If portfolio management were a road trip, the IPS is the map, the budget, the speed limit, and the “no, we are NOT adopting

a raccoon at that gas station” rule. It’s a written guide that ties goals and constraints to how the portfolio will be built,

managed, and reviewed.

A practical IPS typically spells out:

- Objectives: What the money is for (retirement, tuition, long-term growth, income, capital preservation).

- Time horizon: When you need it and how flexible the timeline is.

- Risk tolerance: How much volatility you can live withfinancially and emotionally.

- Constraints: Liquidity needs, taxes, ethical screens, legal restrictions, concentration limits.

- Target asset allocation: The intended mix (like 70/30 or 60/40) and how far it’s allowed to drift.

- Rebalancing rules: When and how you’ll bring the portfolio back to target.

The point isn’t paperwork for its own sake. The point is discipline. A good policy turns “future you” into a calm, rational adult

who can overrule “present you,” who just read an alarming headline and is now convinced the sky is falling (again).

For enterprise portfolios: a governance charter and scoring model

If you manage a portfolio of projects or product bets, your “policy” is the combination of governance, decision rights, and

prioritization criteria. This is where leadership clarifies what “strategic alignment” actually means in practicepreferably with

something more specific than, “It aligns with strategy because… strategy.”

The essentials:

- Decision owners: Who approves, who funds, who can stop work.

- Intake process: How new work enters the system (and how it gets rejected politely).

- Prioritization criteria: Value, risk, time-to-impact, dependencies, regulatory needs, capacity.

- Capacity and funding rules: How resources are allocatedand what happens when reality disagrees with plans.

- Performance measures: Outcomes, benefits realized, and leading indicators (not just “we’re busy”).

In both worlds, the policy is your anchor. It makes decisions consistent, auditable, and harder to hijack by impulse.

Asset Allocation: The Biggest Lever You Control

In investing, asset allocation is the decision about how much you put into broad categoriestypically stocks, bonds, and cash

(and sometimes real assets, alternatives, or other diversifiers). It’s not the flashy part, which is exactly why it matters.

Here’s the truth that sneaks up on a lot of people: asset allocation often matters more than picking individual securities.

That’s because allocation sets the portfolio’s overall risk level and return potential. In plain English: it decides whether you’re

riding a bicycle, driving a sedan, or strapped to a rocket powered by feelings.

Allocation must match goals, not group chats

A retirement portfolio for someone with decades ahead may tolerate more equity risk than a portfolio intended to fund a near-term

home purchase. The bedrock principle is simple: your allocation should be aligned with your objective, time horizon, and risk tolerance.

In enterprise portfolios, “asset allocation” has a cousin: how you allocate capacity and budget across categories like:

- Run vs. Change: Keep-the-lights-on work versus transformation.

- Horizon mix: Short-term wins, medium-term growth, long-term bets.

- Risk buckets: Core improvements versus experimental innovation.

If everything is “top priority,” that’s not prioritizationit’s a cry for help.

Diversification: Don’t Just Own More ThingsOwn Different Things

Diversification is not collecting investments like souvenirs. It’s about reducing the chance that one eventor one segmentwrecks

your plan. A portfolio concentrated in a single stock, sector, or theme can perform brilliantly… right up until it doesn’t.

Diversify across drivers of return

The best diversification isn’t “ten funds that all behave the same.” It’s exposure to different economic drivers: equities versus

high-quality bonds; domestic versus international; large versus small; growth versus value; liquid versus less liquid (with caution).

In project portfolios, diversification looks like balancing:

- Customer-facing growth initiatives and risk-reduction work (security, compliance).

- Revenue bets and cost-saving programs.

- Single-point-of-failure dependencies and parallel paths that create resilience.

A diversified portfolio is not a guarantee of profits. It’s a resilience strategyone that makes outcomes less dependent on a single storyline.

Risk Management: The Adult Supervision Your Portfolio Deserves

Risk management is not pessimism. It’s realism with a seatbelt. The goal isn’t to eliminate risk (impossible); it’s to choose the risks you’re

taking, understand them, and avoid risks you didn’t sign up for.

Common risks you should name out loud

- Market risk: Broad drawdowns that affect most risky assets.

- Concentration risk: Too much exposure to one company, sector, or factor.

- Liquidity risk: Not being able to access cash when needed without major losses.

- Interest-rate risk: Particularly relevant for bonds and rate-sensitive assets.

- Behavioral risk: The tendency to buy high, sell low, and then blame the calendar.

- Operational risk: Implementation mistakes, governance gaps, weak controls, or tool failures.

Enterprise portfolios add risks like dependency chains, resource bottlenecks, vendor concentration, and benefits that exist only

in PowerPoint. Naming risks forces better trade-offsand makes surprises rarer.

Rebalancing: The Portfolio’s Alignment Check (Not a Punishment)

Rebalancing is the act of bringing a portfolio back to its target allocation after markets (or business reality) push it off course.

This matters because drift changes your risk leveloften without permission.

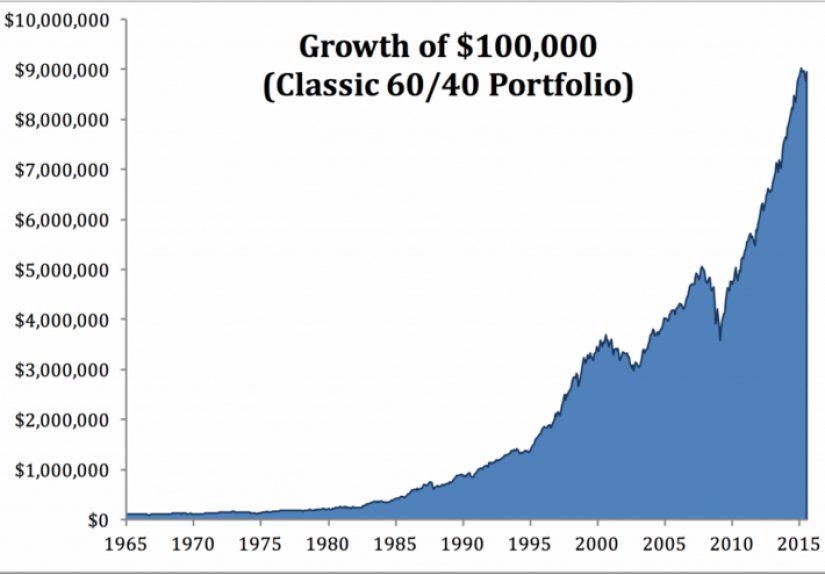

A simple investing example

Imagine you start with a 60/40 mix: 60% stocks, 40% bonds. Stocks rally hard for a few years, and now you’re sitting at 75/25.

Congratulationsyou’re taking much more risk than you planned. Rebalancing means trimming what grew (stocks) and adding to what lagged (bonds)

until you’re back near target.

Rebalancing feels emotionally weird because it often means selling “winners” and buying “losers.” But that’s the whole point:

it pushes you toward discipline rather than chasing performance.

How to rebalance without turning it into a full-time hobby

- Calendar-based: Review quarterly, semiannually, or annually.

- Threshold-based: Rebalance when an asset class drifts beyond a preset band (like 5 percentage points).

- Cash-flow rebalancing: Use new contributions or withdrawals to correct drift before trading.

Enterprise portfolios also rebalancejust with different moves: stopping low-value initiatives, funding high-impact ones, adjusting capacity

across teams, and revisiting the mix as strategy or constraints change.

Costs and Friction: The Silent Returns Thieves

Fees, taxes, and transaction costs rarely trend on social media (because “#expenseRatios” is not a vibe), but they can be brutally important.

Small annual frictions compound. Over decades, they can create a gap that looks less like a rounding error and more like a missing room in your house.

Why “just 1%” can be enormous

Suppose $100,000 grows for 30 years. At 7% annually, it becomes about $761,000. At 6%just one percentage point lowerit becomes about $574,000.

That’s roughly $187,000 of difference over time. Not because anyone stole your money in a dramatic heist… but because compounding is quietly dramatic.

The bedrock rule: control what you can controlfees, unnecessary turnover, avoidable taxes, and sloppy implementation.

Measurement: The Feedback Loop That Keeps You Honest

Good portfolio management uses measurement to make better decisions, not to win arguments at meetings.

For investors: performance in context

- Compare to an appropriate benchmark that matches the portfolio’s risk profile.

- Look at rolling periods (3-, 5-, 10-year) rather than cherry-picked windows.

- Separate process from outcome: a good process can have a bad year; a bad process can get lucky.

For organizations: outcomes, not activity

Enterprise portfolios should measure outcomes like revenue lift, customer retention, cycle time reduction, defect reduction, risk reduction, and

adoptionplus leading indicators that predict whether benefits are likely to show up.

The bedrock principle here is uncomfortable but liberating: if you don’t measure value, you can’t manage value.

Governance: Who Decides, Using What Rules, With What Data?

Governance is where portfolios either become resilientor become political theater. Strong governance clarifies decision rights, review cadence,

escalation paths, and “stop” criteria.

In investing, governance might mean: who can change allocation, what triggers changes, how often the plan is reviewed, and what gets documented.

In enterprise portfolios, governance is often the difference between a strategic portfolio and a backlog with better branding.

What strong governance looks like

- Clear roles: owners, approvers, executors, reviewers.

- Cadence: regular review cycles (not crisis-driven meetings).

- Evidence: decisions based on data and assumptions that can be tested.

- Kill switches: criteria for stopping work that no longer makes sense.

Yes, “kill switches” sound dramatic. But stopping weak initiatives is often the best investment you can makebecause it frees resources for better ones.

A Practical Blueprint: Build a Portfolio That Can Survive Reality

If you want a simple “bedrock” checklist, here it is:

- Write the policy. Define objectives, constraints, decision rights, and review cadence.

- Set the allocation. Choose a mix aligned to goals, horizon, and risk tolerance.

- Diversify intentionally. Spread exposure across different return drivers and failure modes.

- Define risk controls. Limits, stress checks, and “what would break us?” conversations.

- Rebalance with rules. Calendar, thresholds, or cash flowsjust don’t wing it.

- Control costs. Minimize friction that compounds against you.

- Measure what matters. Benchmarks, outcomes, leading indicators.

- Govern like you mean it. Make decisions repeatable, transparent, and reversible when needed.

Portfolio management isn’t a one-time setup. It’s an ongoing practicelike brushing your teeth, except the consequences are more expensive and you can’t

fix them with minty floss.

of Real-World Experience (The Stuff People Learn the Hard Way)

The most common “experience” lesson in portfolio management is that the technical plan is usually finethe human behavior is the wild card. In investing,

plenty of people can explain diversification. Far fewer can stick with it when one part of the portfolio lags for what feels like an eternity (often

a totally normal cycle that just happens to be happening to you).

One recurring real-world pattern: portfolios drift not only because markets move, but because people avoid uncomfortable actions. Rebalancing is a perfect

example. Teams delay it because selling winners feels like betrayal. Buying lagging assets feels like “catching a falling knife.” Yet over time, a rules-based

approach often prevents the portfolio from slowly morphing into a concentrated bet nobody intended to make. The lived experience here is simple: the best time

to decide how you’ll rebalance is when you’re calm, not when you’re caffeinated and doom-scrolling.

In organizations, the parallel experience is that portfolio governance fails when it becomes performative. Leaders hold prioritization sessions, score initiatives,

and declare “focus”then approve everything anyway. The portfolio becomes overcommitted, delivery slows, and the organization concludes (incorrectly) that

“execution is the problem.” In many teams, the breakthrough moment is learning to treat capacity as a real constraint, not a suggestion. When governance includes

explicit trade-offs“If we fund this, what stops?”the portfolio starts behaving like a system instead of a wish list.

Another lesson: measurement has to be usable. Investors learn that obsessing over daily performance can turn long-term planning into short-term anxiety.

Organizations learn that dashboards packed with activity metrics (“tickets closed,” “hours logged,” “projects in flight”) don’t prove value. The mature move is to

pick a handful of measures tied to objectivesbenchmarks and risk metrics for investors; outcomes and benefits for enterprisesand review them consistently.

Finally, everyone learns the “cost” lesson eventually. Investors notice that fees and taxes are the rare enemies you can actually predict. Organizations notice

that context switching, half-funded initiatives, and constant priority changes are also costsjust paid in time, morale, and opportunity. The portfolio that wins

over time is rarely the one with the flashiest ideas. It’s the one that protects focus, follows a process, and makes fewer unforced errors. That’s bedrock in action:

not exciting, not trendy, but incredibly effectivelike a good foundation or a really reliable pair of shoes.

Conclusion: The Bedrock Is Boring on Purpose

The strongest portfolios aren’t built on predictions. They’re built on principles: clear goals, explicit constraints, disciplined allocation and diversification,

risk-aware execution, and a rebalancing habit that keeps reality from drifting into chaos. Whether you’re managing investments or initiatives, the bedrock is the same:

build a system that can survive uncertaintybecause uncertainty is the one thing you can confidently expect.