Table of Contents >> Show >> Hide

- The Good: Why People Keep Coming Back to the Stock Market

- The Bad: Why the Stock Market Can Drive You Crazy

- A Wealth of Common Sense Approach to Stock Investing

- Who Should (and Shouldn’t) Invest Heavily in the Stock Market?

- Practical Tips to Capture the Good and Survive the Bad

- Real-World Experiences: What the Good & Bad Look Like in Practice

- Final Thoughts: Embrace the Trade-Off, Not the Fantasy

If you’ve ever checked your portfolio in the middle of a market sell-off, you already know this truth:

the stock market is both a wonderful money-making machine and a world-class emotional torture device.

The good and the bad come as a package deal. You don’t get long-term growth without short-term chaos,

and you don’t get wealth-building returns without accepting that sometimes your account balance will

look like it fell down a flight of stairs.

In this guide, we’ll walk through the real pros and cons of investing in the stock market, using a

“common sense” lens instead of hype or doom. We’ll talk about why stocks have historically rewarded

patient investors, why they can still feel so risky, and how to build an approach that gives you

the good while surviving the bad.

The Good: Why People Keep Coming Back to the Stock Market

1. Historically Strong Long-Term Returns

Over long periods, broad stock market indexes like the S&P 500 have delivered average annual

returns in the high single digits to around 10% before inflation. That doesn’t mean you earn 10% every

yearfar from it. One year might be +25%, the next might be -15%, and another might be flat. But over

decades, stocks have generally outpaced cash and traditional bonds.

That extra return is called the “equity risk premium”—the reward investors demand for putting up

with scary headlines, price swings, and uncertainty. If you want your money to grow faster than

inflation over a long time horizon, stocks have historically been one of the most reliable ways to do it.

2. Ownership in Real Businesses

When you buy stock, you’re not just buying a line on a chart—you’re buying a slice of a real

business. That business sells products, builds services, hires people, earns profits, and ideally

grows over time. As companies grow their earnings, the value of their shares tends to follow.

This is a key mental shift: you’re not betting on squiggly lines; you’re investing in human creativity,

productivity, and innovation. Over time, that’s a powerful force working in your favor.

3. Dividends and the Magic of Compounding

Many companies share part of their profits via dividends. If you reinvest those dividends back into

more shares, you start compounding—earning returns on your returns. Given enough time, compounding

can turn modest monthly contributions into a very serious nest egg.

The “good” of stock investing isn’t just about high single-year returns. It’s about the snowball

effect that happens when you stay invested, keep adding, and let time do most of the heavy lifting.

4. Liquidity and Flexibility

Unlike real estate or private businesses, publicly traded stocks are usually easy to buy and sell.

Need to rebalance your portfolio? Want to shift from individual stocks to index funds? You can generally

do that in seconds during market hours.

This liquidity is part of what makes the stock market so useful: you get access to thousands of

companies, sectors, and strategies, and you can shift your mix as your goals, income, or risk tolerance

change.

The Bad: Why the Stock Market Can Drive You Crazy

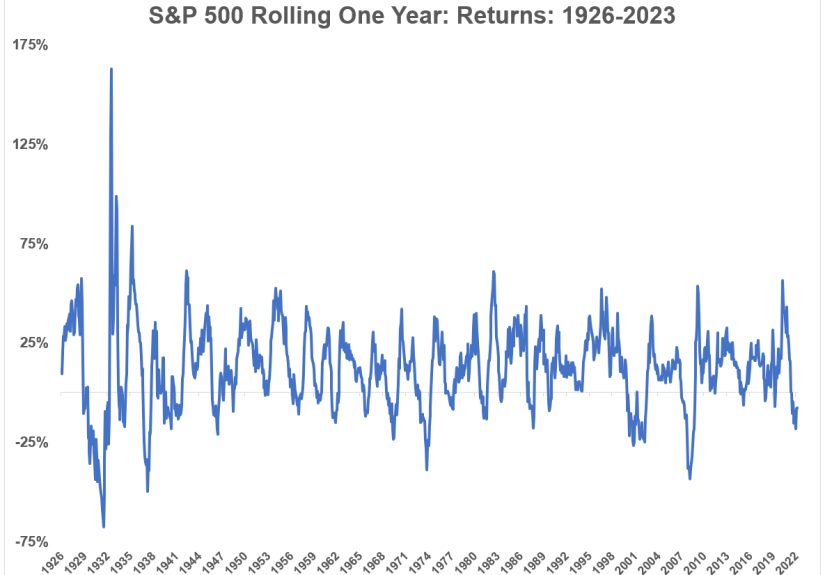

1. Volatility and Gut-Wrenching Drawdowns

The catch with all those attractive long-term returns is that the road is anything but smooth. In a

typical year, the stock market can experience multiple pullbacks of 5–10%. Every few years, you’ll see

something closer to a 20%+ drop (a bear market). Occasionally, you get a true crash where prices fall

30–50% or more.

On a long-term chart, those dips can look like minor bumps. In real life, they feel like a financial

horror movie. If you’re not prepared, volatility can tempt you into selling at exactly the wrong time.

2. Timing Risk and “Bad Start” Risk

Another unpleasant reality: when you start investing matters, especially over shorter horizons. If

you invest a lump sum right before a bear market, you can spend years just getting back to breakeven.

That’s painful if you need the money soon, or if you let early losses permanently scare you away

from the market.

For long-term savers who are adding money steadily (for example, every month into a retirement

account), rough markets can actually be a hidden blessing because they let you buy more shares at

lower prices. But emotionally, that opportunity often feels like punishment, not a discount.

3. You Are Probably Your Own Worst Enemy

The math of the stock market is one thing; the psychology is another. A long list of behavioral

biases tends to trip investors up: overconfidence, loss aversion, herd mentality, recency bias,

and good old-fashioned fear and greed.

Common patterns include:

- Buying after big run-ups because “everyone else is getting rich.”

- Selling after big drops because “this time is different and it will never recover.”

- Trading too often, chasing hot tips, and under-diversifying into a few favorite names.

- Ignoring costs and taxes, which quietly eat into returns.

Historically, these behaviors cause many investors to underperform the very funds they invest in,

simply because they buy and sell at the wrong times. The market’s bad days are unavoidable. Bad

decisions, however, are optional (even if they’re tempting).

4. Single-Stock Risk vs. Market Risk

There’s a big difference between owning a diversified index fund and betting your savings on a few

individual stocks. While the overall market has historically trended upward over long periods, many

individual companies do not. Some stagnate for years; others go to zero.

Research on global stocks has shown that a relatively small percentage of companies create the bulk

of total market wealth. That means stock pickers who aren’t diversifying broadly run the risk of

missing the big winners and overexposing themselves to the losers.

A Wealth of Common Sense Approach to Stock Investing

1. Accept That You Don’t Get the Good Without the Bad

One of the central ideas behind the “wealth of common sense” style of investing is simple: the good

stuff and the bad stuff are inseparable. You don’t get higher long-term returns without tolerating

short-term pain. You can’t expect to grow wealth in stocks while also demanding that prices never

fall.

That means the goal isn’t to avoid volatility entirely; it’s to choose a level of volatility that

your stomach and your financial plan can handle. The right portfolio is the one you can stick with,

not the one that looks the best in a backtest.

2. Simplicity Usually Beats Cleverness

Many investors spend years hopping between complex strategies, exotic products, and hot trends, often

with disappointing results. Meanwhile, plenty of people quietly build wealth by doing something much

simpler:

- Owning low-cost, diversified stock index funds.

- Pairing them with safer assets (like high-quality bonds or cash) for stability.

- Contributing regularly, regardless of headlines.

- Rebalancing once or twice a year.

It isn’t flashy. It doesn’t sound like something you’d brag about at a party. But for most people,

simple, rules-based investing has a much higher success rate than attempts to outsmart the market

every week.

3. Respect the Benchmark: Most Pros Don’t Beat It

A useful reality check: over long periods, the majority of actively managed mutual funds fail to

outperform broad benchmarks like the S&P 500 after fees. If full-time professionals with teams,

data, and supercomputers struggle to beat the market, it’s worth asking how realistic it is for a

busy individual investor to do it consistently.

That’s why legendary investors like Warren Buffett have repeatedly recommended low-cost index funds

for most people. The idea is not that the market is perfect, but that for the average investor,

“good enough” with low costs and low stress beats heroic attempts to be a market genius.

Who Should (and Shouldn’t) Invest Heavily in the Stock Market?

Good Candidates for Significant Stock Exposure

- Long-term savers with a time horizon of 10+ years (retirement, kids’ college, etc.).

- People with stable income who can keep investing through downturns without needing to sell.

- Investors with emergency funds who don’t need to raid their portfolios when life happens.

- Folks who can tolerate seeing red numbers without immediately hitting the sell button.

People Who May Want a Lower Stock Allocation

- Those nearing retirement who will soon rely on their portfolio for monthly income.

- Anyone who loses sleep over day-to-day price swings.

- People who need the money within a few years (for a house, tuition, or major life event).

You don’t have to choose “all stocks” or “no stocks.” Asset allocation is a spectrum. A 25-year-old

might be comfortable with 80–90% in stocks. A 65-year-old might prefer 40–60%. The key is matching

your mix to your time horizon, cash flow needs, and emotional wiring.

Practical Tips to Capture the Good and Survive the Bad

1. Start with a Plan, Not a Hot Tip

Decide on your goals, time horizon, and risk tolerance first. From there, build a target allocation

(for example, 70% stocks / 30% bonds) that fits your situation. If you skip this step and just chase

whatever’s hot, the market will eventually give you a very expensive education.

2. Diversify Broadly

Instead of betting on a handful of companies or sectors, use broad index funds that hold hundreds or

thousands of stocks. Diversification won’t prevent losses in a market-wide downturn, but it can reduce

the risk of any single bad pick wrecking your finances.

3. Automate Contributions and Rebalancing

Set up automatic transfers into your investment accounts every month. Treat it like a bill you pay to

your future self. Then, once or twice a year, rebalance back to your target allocation. That way you

systematically “sell high and buy low” without overthinking it.

4. Limit How Often You Check Your Account

The more often you look at your portfolio, the more volatility you feel. Daily swings that are normal

statistically can feel terrifying emotionally. Consider checking in on a schedule—monthly or

quarterly—instead of reacting to every headline.

5. Prepare for Bad Markets in Advance

At some point, you will live through another bear market. That’s not a prediction; it’s a feature of

how markets work. Decide in advance how you’ll respond:

- How much are you willing to see your portfolio drop without changing your plan?

- Will you keep contributing even when things look bleak?

- What percentage decline would genuinely be too much for you?

Writing this down can help you stay calm when the bad times arrive. Panic loves surprise. Preparation

takes away some of its power.

Real-World Experiences: What the Good & Bad Look Like in Practice

To make all this less abstract, let’s look at a few common experiences that many investors have lived

through—and the lessons they offer.

Case 1: The New Investor Who Started Right Before a Crash

Imagine a 28-year-old who finally gets serious about money and invests a lump sum into a broad U.S.

stock index fund. Two months later, a global crisis hits and the market drops 30%. Our investor

feels sick. “I did everything ‘right’ and now my savings are getting crushed.”

There are two possible paths from here. In the bad version, they sell near the bottom, lock in their

losses, and stay out of the market for years, missing the eventual recovery. In the better version,

they keep contributing monthly, buying more shares at cheaper prices. Years later, the painful start

ends up being a blessing because most of their dollars were invested at lower valuations.

The lesson: the bad of stock investing often shows up early and loudly. But if you keep adding over

time, rough beginnings don’t have to ruin your long-term outcome.

Case 2: The Long-Term Saver Who Ignored the Noise

Picture someone who started investing in the early 2000s. They lived through the dot-com bust, the

2008 financial crisis, the 2020 pandemic crash, and multiple corrections in between. If they had

reacted to every scary headline by going to cash, they would have spent most of their investing life

on the sidelines.

Instead, suppose they:

- Kept a simple mix of stock and bond index funds.

- Invested a set amount every month, no matter what.

- Rebalanced occasionally but didn’t try to time the market.

After two decades, that boring, consistent behavior would likely have produced a portfolio far larger

than they imagined at the start. The good of long-term compounding ultimately outweighed the bad of

scary, temporary declines.

Case 3: The Trader Who Confused Luck with Skill

Now consider the opposite story. During a hot bull market, someone starts trading individual stocks,

options, and trendy themes. At first, it goes great. They catch a few big winners and their account

doubles. They attribute this to their “edge” rather than a roaring market lifting almost everything.

When conditions change, volatility spikes and the themes they loved fall out of favor. They double

down to “win it back,” trade more often, and take on more leverage. Eventually, they experience the

bad side of concentrated risk: a huge drawdown or a blow-up that wipes out years of gains.

The lesson: the stock market can reward risky behavior for a while, which makes it dangerously

addictive. But over the long run, common sense and risk management usually beat adrenaline.

Putting the Experiences Together

These stories are simplified, but they capture a pattern. The good of stock investing shows up for

people who:

- Use diversified, long-term strategies.

- Match their risk to their real-life needs.

- Stay consistent through both good and bad markets.

The bad tends to dominate when investors:

- Confuse speculation with investing.

- Let emotions drive their decisions.

- Take on more risk than they can handle in real life.

Ultimately, the stock market is neither friend nor enemy. It’s a powerful tool. Used with a “wealth

of common sense,” it can help you build real, lasting financial security. Used carelessly, it can

become a very expensive teacher.

Final Thoughts: Embrace the Trade-Off, Not the Fantasy

The good and bad of investing in the stock market are intertwined. You get:

- Higher long-term return potential and uncomfortable short-term volatility.

- The chance to grow wealth faster than inflation and the risk of scary drawdowns.

- A simple path to financial independence and the challenge of managing your own behavior.

The fantasy is that there’s some secret strategy that gives you all of the upside with none of the

downside. The reality is more grounded: pick a sensible stock allocation, diversify, keep your costs

low, automate your contributions, and stick with your plan through both bull and bear markets.

Do that, and you give yourself a great chance to enjoy the good of stock investing while keeping the

bad to a level your nerves — and your sleep — can handle.