Table of Contents >> Show >> Hide

- 2019 Was a Monster Year, but Not for Just One Reason

- Big 2019 Returns Also Meant Higher Expectations for 2020

- What History Suggested About Following a Big Year

- Why Diversification Looked Smarter Going Into 2020

- The 2020 Election Added a Layer of Noise

- What Big 2019 Returns Really Meant for Investors

- Specific Examples Investors Could Watch in 2020

- Conclusion: 2019 Was a Gift, Not a Guarantee

- Experiences Investors Carried From 2019 Into 2020

Wall Street did not just have a good 2019. It had a “check your portfolio twice because that can’t be right” kind of 2019. After the ugly sell-off at the end of 2018, U.S. stocks came roaring back. The S&P 500 delivered one of its best years of the decade, the Nasdaq sprinted ahead like it had a double espresso, and the Dow reminded everyone that old blue chips still know how to dance.

So what did those big stock market returns in 2019 actually mean for 2020? Did they signal another easy year of gains? Did they warn investors that stocks were getting expensive? Or were they simply the market’s way of saying, “Congrats on surviving 2018, here’s your rebound?”

The real answer sits somewhere in the middle. Huge returns in one year rarely hand out promises for the next one. What they do offer is context. They show what powered the rally, what risks got ignored, what expectations got baked into prices, and what investors needed to watch carefully as the calendar flipped to 2020.

2019 Was a Monster Year, but Not for Just One Reason

To understand what 2019 meant for 2020, it helps to start with why stocks surged in the first place. This was not a one-button rally. It was more like a carefully stacked sandwich of relief, policy support, and investor optimism.

The market rebounded from a nasty 2018 finish

One of the biggest reasons stocks posted such impressive 2019 returns is that they started from a wounded position. The late-2018 sell-off left investors nervous about global growth, Federal Reserve tightening, and trade tension between the United States and China. That lower starting point gave the market room to bounce. In plain English, when stocks fall into a hole and then climb out, the percentage gain can look dramatic.

This matters because some of 2019’s performance was recovery, not fresh economic magic. Investors entering 2020 had to ask an uncomfortable question: how much upside had already been pulled forward?

The Federal Reserve changed the mood

The Fed played a huge role in changing investor psychology. In 2019, the central bank shifted from tightening to easing, cutting interest rates three times. Lower rates tend to support higher stock valuations because they reduce borrowing costs, make bonds less competitive, and encourage investors to take more risk. Suddenly, the market’s soundtrack changed from “brace for impact” to “maybe we can relax for five minutes.”

For 2020, that meant one key thing: investors could not count on the same level of surprise support again. Easier monetary policy had already done a lot of heavy lifting. If stocks were going to keep rising, the next leg higher would likely need help from better earnings, steadier growth, or both.

Trade worries eased just enough

The trade war did not vanish in 2019, but it stopped acting like a daily horror movie trailer by year-end. Progress toward a Phase One trade deal helped calm markets and reduce fears that tariffs would keep choking business confidence. That easing in tension helped investors look past manufacturing weakness and focus on the possibility of stabilization.

Heading into 2020, that meant markets were pricing in less chaos. The upside case depended on more follow-through, not just fewer scary headlines. If trade tensions stayed manageable, stocks had a chance to grind higher. If negotiations fell apart again, investors might discover that optimism had been a little overbooked.

Big 2019 Returns Also Meant Higher Expectations for 2020

When a market delivers a year as strong as 2019, it does not just make investors richer. It also makes them pickier, greedier, and occasionally a little too confident. That is human nature. It is also portfolio management’s least charming personality trait.

Valuations became more important

A major lesson from 2019 was that stock prices rose much faster than corporate profits. Earnings growth was weak compared with the size of the rally, meaning a large part of the advance came from investors becoming willing to pay more for each dollar of earnings. That is called multiple expansion, and it is great while it lasts. It is less great when expectations get ahead of reality.

For 2020, this raised the stakes. Stocks were no longer cheap rebound plays. They were becoming more expensive assets that needed stronger fundamentals to justify further gains. In other words, 2020 was shaping up to be less about “the Fed saved the mood” and more about “show me the earnings.”

The bar for corporate profits got higher

Analysts going into 2020 generally expected earnings growth to improve after a sluggish 2019. That view made sense on paper. Comparisons were easier, recession fears had cooled, and lower rates were supportive. But when a market already has a big rally behind it, decent earnings are not always enough. Investors start demanding better-than-expected results, stronger guidance, and proof that margins can hold up.

This is one of the clearest meanings of the 2019 rally: 2020 would likely be a year where fundamentals mattered more. Stocks might still rise, but it would probably be harder work.

What History Suggested About Following a Big Year

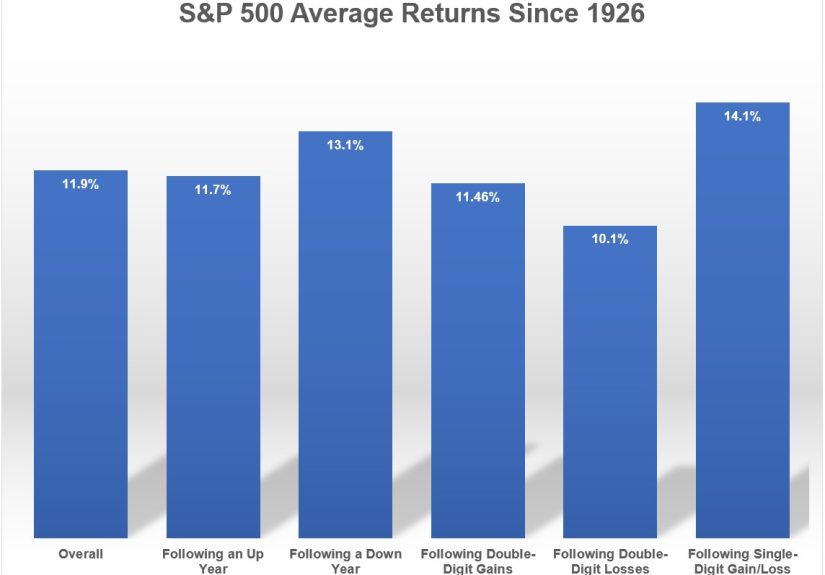

Investors love asking whether a huge year automatically leads to another huge year. History, as usual, responds with a shrug. Strong gains do not guarantee a slump, but they also do not create a coupon for another 30% return. Markets are not loyalty programs.

After major rallies, future returns often become more modest because valuations are higher and good news is already reflected in prices. That does not mean a bear market is inevitable. It means the odds shift. The market may keep moving up, but investors should expect more volatility, more sensitivity to earnings misses, and more hand-wringing over every headline that sounds remotely macroeconomic.

For 2020, that historical pattern pointed toward a likely scenario of positive but lower returns than 2019, assuming the economy avoided recession. That was, in fact, a common theme among market outlooks at the time. Plenty of strategists expected gains, but few expected another effortless moonshot.

Why Diversification Looked Smarter Going Into 2020

Another thing big 2019 stock market returns meant for 2020 was that investors needed to think more carefully about concentration risk. Technology stocks were major leaders in 2019, and large-cap U.S. companies did especially well. That was wonderful if you owned the winners. It also created a subtle trap: assuming yesterday’s leadership would automatically keep carrying the market forever.

Several investment outlooks entering 2020 emphasized diversification for exactly this reason. When U.S. stocks have already had a huge run and valuations are elevated, opportunities sometimes broaden to other asset classes, other regions, or parts of the market that were left behind. Bonds had also delivered strong returns in 2019, thanks in part to falling yields, which reminded investors that balanced portfolios were not just decorative accessories.

So if 2019 was the year of broad relief and big cap leadership, 2020 looked more like a year when being diversified could matter again. Not because diversification is glamorous, but because it saves investors from turning a portfolio into a fan club.

The 2020 Election Added a Layer of Noise

As if investors did not already have enough to obsess over, 2020 was also a U.S. presidential election year. Election years tend to invite all kinds of hot takes, dramatic forecasts, and financial TV panels featuring people who look deeply concerned in expensive ties.

The lesson from 2019’s rally was not that politics would suddenly dominate returns. It was that markets heading into 2020 had less room for disappointment. When stocks are richly valued and coming off a huge year, election-related uncertainty can create sharper reactions even if the long-term effect turns out to be limited.

That meant investors in 2020 needed to separate noise from signal. Tax policy, regulation, health care, trade, and fiscal spending all mattered. But the bigger drivers were still the same familiar trio: growth, earnings, and interest rates.

What Big 2019 Returns Really Meant for Investors

If we boil the whole story down to its essentials, the message of 2019 for 2020 was pretty clear.

First, the market had already used up a lot of easy upside. Second, low rates and easing trade fears created support, but they were not infinite fuel tanks. Third, earnings growth needed to improve for stocks to justify moving significantly higher. And fourth, investors should expect a less forgiving market, where valuation, sector leadership, and macro headlines could matter more than they did during the rebound phase.

That is not a gloomy message. It is a realistic one. Big market returns are exciting, but they often change the next year’s job description. After a rebound year, the market usually asks for receipts.

Specific Examples Investors Could Watch in 2020

Large-cap technology

Technology helped lead 2019’s rally, so 2020 naturally brought questions about whether the sector could keep outperforming. The answer depended on earnings durability. If revenue growth and margins stayed strong, leadership could continue. If expectations outran business reality, even strong companies could face pressure.

Financials

Financial stocks had reasons for optimism, including a healthy consumer and stable credit conditions. But lower interest rates also pressured net interest margins. That made 2020 more of a stock-picker’s environment than a simple “buy the whole sector and celebrate” situation.

Industrials and cyclicals

These areas had lagged at times when trade tension and manufacturing weakness dominated headlines. If the global economy stabilized in 2020, cyclicals had room to recover. That is one reason many investors entered the year watching for a broader market rally beyond the obvious winners.

Conclusion: 2019 Was a Gift, Not a Guarantee

The giant stock market returns of 2019 meant something important for 2020, but not something magical. They did not guarantee a crash. They did not promise another blockbuster year either. What they really signaled was a transition.

The market was moving from rebound mode into expectation mode. In rebound mode, relief does most of the work. In expectation mode, investors start demanding proof. They want better earnings, steadier growth, and fewer policy shocks. They become more sensitive to valuation and less patient with excuses.

That made 2020 look, at the start, like a year for discipline more than drama. The smart takeaway from 2019 was not to chase whatever had already gone vertical. It was to recognize that strong returns are wonderful, but they often leave behind a tougher test. The market had recovered. Now it had to earn its confidence all over again.

Experiences Investors Carried From 2019 Into 2020

If you were investing around the handoff from 2019 to 2020, the experience probably felt a little surreal. Just a year earlier, many investors had ended 2018 with that classic feeling of “maybe I should check my retirement account sometime in the next century.” Then 2019 arrived and turned fear into confidence with almost suspicious speed. By December, the emotional mood of the market had changed so much that people who had been panicking twelve months earlier were suddenly wondering whether they should add more stocks because everything looked unstoppable.

That emotional swing is one of the most important real-world lessons tied to the topic. Markets do not just move money. They move behavior. After a big year like 2019, investors often feel smarter than they really are. Gains create comfort, comfort creates confidence, and confidence sometimes creates very creative explanations for why risk no longer exists. Spoiler: risk always exists. It just changes outfits.

Many investors also experienced a form of delayed regret. Those who sold during the rough finish to 2018 had to watch the rebound from the sidelines. That can be more painful than losing money in the first place, because it combines missed gains with bruised pride. The lesson is not that investors should never reduce risk. It is that emotional decisions made during panics often look especially expensive once the market recovers.

On the flip side, investors who stayed invested through 2019 learned a very different lesson. They saw that markets can recover long before the headlines feel comfortable. The economy did not look flawless. Trade fights were still happening. Manufacturing data was shaky. Analysts were debating recession risks. And yet stocks kept climbing. That experience reinforced an old truth that many people only believe after living through it: the stock market is forward-looking, impatient, and completely willing to rally while everybody is still arguing about the latest scary chart.

There was also a practical experience tied to portfolio construction. Investors who had diversification in place often felt less pressure to make dramatic moves. They could rebalance. They could trim winners. They could add to lagging areas without turning every decision into a full-blown identity crisis. Investors who were heavily concentrated in the hottest names sometimes had a rougher emotional ride, even if they made more money, because every earnings report started to feel like a high-stakes final exam.

By the start of 2020, the lived experience of 2019 had taught disciplined investors a few valuable things: rebounds can happen faster than expected, central bank policy matters more than most people want to admit, valuations eventually matter again, and emotional whiplash is part of the investing package whether you ordered it or not.

Most of all, the 2019-to-2020 transition reminded investors that a great year should inspire gratitude, not laziness. Big returns are wonderful, but they can tempt people into confusing momentum with certainty. The healthiest mindset going into any new year is not “the market owes me another win.” It is “that was a strong year, now what assumptions am I making, and are they actually reasonable?” That question is not flashy, but it has saved a lot more portfolios than blind optimism ever has.

Note: This is clean, publish-ready HTML body content in standard American English, with no source links and no unwanted oaicite or contentReference artifacts.