Table of Contents >> Show >> Hide

- Thought #1: This is why you own bonds

- Thought #2: The machines didn’t create volatility

- Thought #3: Most people probably shouldn’t try to buy low and sell high

- Thought #4: It’s for the best (yes, really)

- Thought #5: There isn’t just one reason

- A Market Downturn Mini-Playbook (practical, not magical)

- Frequently Asked “Downturn Questions” (the ones people whisper at 2 a.m.)

- Experience Notes: What Market Downturns Feel Like in Real Life (and why that’s normal)

- Conclusion: Common Sense Beats Perfect Timing

A market downturn has a special talent: it turns perfectly reasonable people into doom-scrollers with a finance app open in one hand and a stress snack in the other.

Suddenly, every headline feels personal. Your portfolio feels like it’s “doing something,” and that something is auditioning for a tragedy.

Here’s the good news (and it’s very on-brand for “wealth of common sense”): downturns are not a glitch in the system. They’re the system.

Prices move. Investors panic. Markets recover. Repeat for a few centuries.

This article expands on Ben Carlson’s classic “5 Thoughts on the Market Downturn” framework and adds practical, modern contextwithout pretending we can predict next week.

We’ll keep it honest, specific, and a little funny, because laughter is cheaper than therapy (though both can be excellent diversifiers).

Thought #1: This is why you own bonds

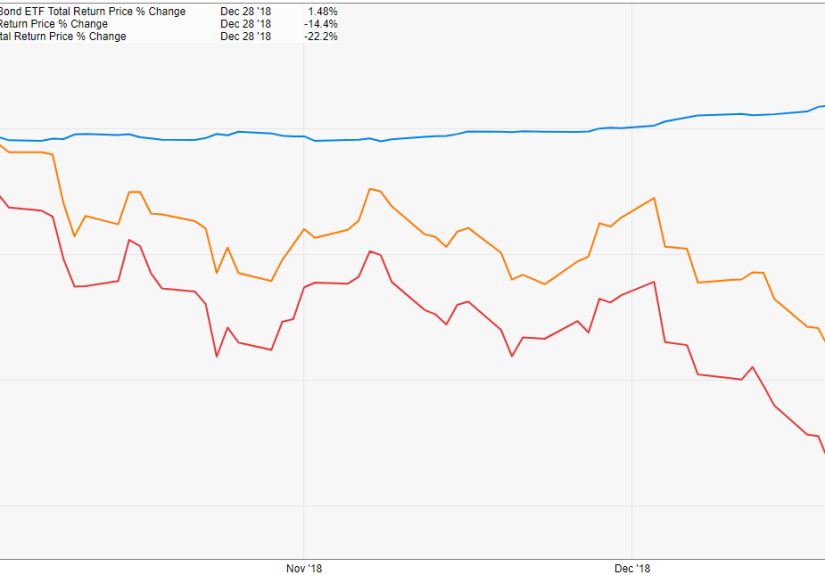

When stocks drop, bonds often become the portfolio’s designated adult in the room. Not because bonds are exciting (they’re not), but because their job is different.

Stocks are the growth engine. Bonds are the shock absorbers. If your portfolio were a car, stocks are the horsepower and bonds are the seatbelt.

What bonds really do in a downturn

- They can reduce the emotional whiplash. Lower overall volatility can make it easier to stick with your plan.

- They can be a “safe-ish” landing spot. In some sell-offs, high-quality bonds may hold up better than stocks.

- They can act as dry powder. You can rebalance by selling some bonds to buy stocks after stocks fallwithout having to “find cash” at the worst moment.

Notice what’s missing: “Bonds always go up when stocks go down.” That’s not a law of nature. Sometimes stocks and bonds both have a rough stretch.

But a balanced mix can still lower the chance that your entire portfolio gets punched in the face at the same time.

A simple example (numbers beat vibes)

Imagine a portfolio that’s 70% stocks and 30% high-quality bonds. If stocks fall 20% and bonds are flat, the portfolio is down about 14%.

That’s still unpleasantbut it’s less “why do I feel faint?” than a 100% stock portfolio that’s down the full 20%.

And here’s the sneaky benefit: the more manageable the decline feels, the more likely you are to stay investedwhich is the whole game.

If bonds help you avoid panic-selling, they might earn their keep even if they never become the life of the party.

Thought #2: The machines didn’t create volatility

When markets get messy, people love a villain. Algorithms! High-frequency traders! The moon phase! (Okay, not that last one… usually.)

But volatility existed long before computers were doing math at warp speed.

Computers can amplify moves, sure. But they didn’t invent fear, greed, overconfidence, or “I just read a thread that ends with rocket emojis.”

Humans created the machinesand humans still supply the emotions that make markets swing.

Why this matters

If volatility is a permanent feature of markets, then the correct response is not “How do I eliminate volatility?”

The correct response is: “How do I build a plan that can survive volatility?”

- Expect big moves. Not every year, not every monthbut often enough that you shouldn’t be surprised when it happens.

- Design your portfolio around your reality. If a 30% drop would make you bail, you’re not “weak,” you’re humanadjust the risk before the panic arrives.

- Focus on behavior, not brilliance. Most long-term investing success comes from avoiding unforced errors.

Think of it like storm-proofing a house. You don’t scream at the weather. You check the roof, secure the windows, and keep a flashlight.

Markets are weather. Your plan is the house.

Thought #3: Most people probably shouldn’t try to buy low and sell high

“Buy low, sell high” is excellent advice in the same way “eat less, move more” is excellent health advice.

Simple. True. Also… not exactly a step-by-step strategy for real humans living real lives with real emotions.

The tough part isn’t understanding the sentence. It’s recognizing “low” when everyone is shouting that the world is ending,

and recognizing “high” when everyone is convinced this time is different (again).

A more usable version of the advice

For many investors, a better rule is:

Buy whenever you have long-term money to invest, and sell only when your plan says you need tofor goals, for rebalancing, or for life.

That can look like:

- Automatic investing (like a consistent monthly contribution), so you’re not negotiating with your fear every time the market sneezes.

- Rebalancing rules (calendar-based or threshold-based), so “buy low” becomes a process, not a personality trait.

- A clear time horizon for each goal, so you’re not using “next year’s tuition money” as your emergency bravery fund.

Why market timing is so punishing

The market tends to deliver some of its biggest up days around the same time as its ugliest down days. That’s not poeticit’s inconvenient.

If you jump out during the scary part, you can easily miss the rebound that follows. And missing a small number of the market’s best days

can meaningfully reduce long-term returns.

The takeaway isn’t “never make a change.” The takeaway is: don’t confuse a temporary emotion with a permanent strategy.

A plan should be boring. Panic is already exciting enough.

Thought #4: It’s for the best (yes, really)

Nobody likes market downturns. But over the long run, downturns serve a purpose:

they remind everyone that risk is the entry fee for higher expected returns.

If stocks only went up in a neat straight line, stocks wouldn’t pay a premium. They’d be a savings account with better branding.

The uncomfortable swings are part of why long-term investing can work.

Downturns can help in three weirdly helpful ways

- They reset expectations. When markets feel invincible, people take dumb risks. A downturn is a cold shower.

- They create future opportunity for savers. If you’re still contributing to your investments, lower prices can mean better forward-looking returns than buying at peak hype.

- They pressure-test your plan. If your strategy only works when everything goes perfectly, it isn’t a strategyit’s a wish.

Important nuance: a downturn is not “good” in the moment. It can hurt. It can last longer than you want.

But if you’re investing for the long term, the presence of downturns is not evidence your plan is broken. It’s evidence your plan is alive.

Thought #5: There isn’t just one reason

Markets love stories. Investors love stories. Financial TV especially loves storiespreferably with a villain, a hero, and a countdown clock.

But big market moves rarely come from one single cause.

In reality, markets are a chaotic blender of:

- interest rates and inflation expectations,

- economic growth and corporate profits,

- geopolitics and policy uncertainty,

- positioning, leverage, and forced selling,

- investor sentiment, fear, and momentum.

That’s why the headline explanation often changes week to week. “It’s the Fed.” “It’s earnings.” “It’s oil.” “It’s AI.”

Sometimes it’s all of the above. Sometimes it’s none of the above and the market just needed to exhale.

Common-sense response to messy causes

If you can’t reliably explain a downturn in real time (and almost nobody can), then building a strategy around precise predictions is… ambitious.

A sturdier approach is to focus on what you can control:

your savings rate, your diversification, your fees, your tax strategy (if relevant), andmost importantyour behavior.

A Market Downturn Mini-Playbook (practical, not magical)

1) Separate “money soon” from “money later”

If you need money in the next few years, it generally shouldn’t be exposed to full stock-market risk.

The market does not care about your timeline. (Rude, but consistent.)

Match the risk level to the goal’s deadline.

2) Rebalance with rules, not moods

Rebalancing is the grown-up version of “buy low, sell high.” It’s not a prediction; it’s maintenance.

When stocks fall and bonds rise (or fall less), rebalancing can nudge you to buy stocks when they’re cheaper and trim what’s become oversized.

Two common approaches:

- Calendar rebalancing: Check once or twice a year and reset to target allocations.

- Threshold rebalancing: Rebalance when an allocation drifts beyond a set band (for example, 5 percentage points).

3) Keep a real emergency fund (so you don’t liquidate at the worst time)

A downturn is annoying. A downturn plus an unexpected expense is how people get forced into selling at bad prices.

An emergency fund isn’t an “investment.” It’s a stress-reduction device that protects your long-term investments from short-term life.

4) Reduce “decision frequency”

Checking your portfolio constantly doesn’t make you safer. It often makes you jumpier.

If you must check, consider checking less often or focusing on what you can control (contributions, diversification, debt payments) instead of daily price swings.

5) If you’re unsure, simplify

Complicated strategies can fall apart under stressespecially if you don’t fully understand them.

A diversified, low-cost portfolio you can stick with is usually more powerful than a fancy strategy you abandon in a panic.

Friendly note: This is educational content, not personalized financial advice.

If you’re investing with a parent/guardian or using a custodial account, talk decisions through togetheror with a licensed professional.

Frequently Asked “Downturn Questions” (the ones people whisper at 2 a.m.)

“Should I wait for things to calm down before investing?”

Calm is usually more expensive than chaos. By the time things “feel safe,” prices may have already risen.

If you’re investing for the long term, a consistent approach (like dollar-cost averaging) can reduce the pressure to pick a perfect day.

“What if this time is different?”

Every downturn has a unique storylineand the feelings are always familiar: fear, uncertainty, regret, the urge to do something dramatic.

The more useful question is: “Is my plan built for difficult markets?” If yes, stay disciplined. If no, adjust when you’re calm, not when you’re cornered.

“How do I know if I’m taking too much risk?”

One test: imagine your portfolio drops 25% and stays down for a while. Would you stick to the plan and keep investing?

If you’d likely bail, you may need more diversification and a risk level that matches your ability to stay invested.

Experience Notes: What Market Downturns Feel Like in Real Life (and why that’s normal)

The internet is packed with “what you should do” during a downturn. But what matters is what people actually feelbecause feelings drive actions,

and actions drive results. Below are common, real-world experiences investors frequently report during downturns, presented as composite scenarios

(not anyone’s private story). If any of these sound familiar, congratulations: you are experiencing the ancient human tradition of being a human.

Experience #1: The “I’m fine… I’m fine… I’m not fine” phase.

Early in a downturn, many investors feel mildly annoyed. Then the decline deepens and the emotional temperature rises.

A 5% drop can feel like a headline. A 15% drop can feel like a personality test. People often notice they start checking accounts more frequently,

reading more financial news, and interpreting every market bounce as “the bottom” (or every new dip as “the end”).

The key learning: the urge to monitor is usually strongest when monitoring is least helpful.

Experience #2: The “sell to stop the pain” temptation.

In sharper sell-offslike those seen during major crisessome investors feel a powerful desire to sell “just until things settle.”

This is where bonds, cash reserves, and a written plan earn their keep.

Investors who have a mix of assets often describe a strange comfort: even if the portfolio is down, it doesn’t feel like everything is breaking at once.

That emotional buffer can be the difference between staying invested and turning a temporary paper loss into a permanent one.

Experience #3: The “I waited too long… now I’ll wait a bit more” trap.

Another common experience is freezing. Investors don’t sell, but they stop contributing.

They tell themselves they’ll resume investing “when the market is more stable,” but markets rarely send a polite invitation that says,

“Hello, stability has arrivedplease re-enter at your convenience.”

Many people later realize the contributions they skipped during the downturn were the ones that could have bought more shares at lower prices.

The learning isn’t to be fearlessit’s to use automation and simple rules so courage isn’t required every month.

Experience #4: Rebalancing feels backwards (because it is).

Investors who rebalance during downturns often describe it as emotionally weird.

You’re selling something that “did okay” to buy something that “is failing.” That’s exactly why it works as a discipline:

it forces you to buy what’s become cheaper and trim what’s become relatively more expensive.

People who adopt a rebalancing rule say the rule becomes a reliefbecause it turns a scary decision into a routine task.

Experience #5: The rebound is usually messier than the panic.

When markets recover, it’s often not a clean V-shape with fireworks.

It can be a jagged climb with fake-outs, scary headlines, and days where it feels like we’re right back in trouble.

Investors who stayed invested often report the rebound felt “unreal” at firstlike it couldn’t possibly last.

That uncertainty is normal. The point is not to feel confident. The point is to keep showing up anyway.

Experience #6: People learn what their real risk tolerance is.

A downturn reveals the difference between “I think I can handle risk” and “I can actually handle risk.”

Plenty of investors discover they were overexposednot because they were reckless, but because markets were calm for so long that risk felt abstract.

After the downturn, many build a sturdier setup: a more balanced allocation, a bigger emergency fund, fewer speculative bets,

and a commitment to simpler, repeatable behavior.

If there’s one “experience-based” lesson that beats all the clever tactics, it’s this:

the best plan is the one you can stick with when you’re stressed.

During downturns, investing stops being a math test and becomes a psychology test.

And the highest score usually goes to the person who does the most boring thing possible:

they stay diversified, rebalance when needed, keep contributing if their timeline allows, and refuse to outsource their brain to headlines.

Conclusion: Common Sense Beats Perfect Timing

Market downturns will keep happening. The stories will change, the charts will look different, and the panic will recycle with fresh packaging.

But the common-sense response stays remarkably stable:

diversify, use bonds for balance, avoid dramatic timing attempts, rebalance with rules, and accept that volatility isn’t a bug.

If you want a single sentence to tape to your monitor, try this:

“I don’t need to predict the downturn; I need a plan that can live through it.”