Table of Contents >> Show >> Hide

- What Is Empower Personal Cash?

- Quick Verdict

- What Empower Personal Cash Does Well

- Where Empower Personal Cash Falls Short

- How Empower Personal Cash Compares to a High-Yield Savings Account

- Who Should Open Empower Personal Cash?

- Who Should Probably Pass?

- My Take on the Real User Experience

- Experience-Based Scenarios: What It Feels Like in Real Life

- Final Verdict

- SEO Tags

If your money is sitting in a sleepy checking account earning almost nothing, Empower Personal Cash will try very hard to look like the hero in this story. And, to be fair, it has a decent case. It is a cash management account designed for people who want a better place to park idle cash without jumping through the usual flaming hoops of monthly fees, minimum balance rules, and “surprise, we got you” fine print.

But this is not a magical unicorn bank account that does everything. Empower Personal Cash works best as a high-yield cash hub, not as a full replacement for a traditional checking account. That distinction matters. A lot. If you walk in expecting debit card swipes, paper checks, and a full old-school bank branch vibe, you may end up looking confused in the cereal aisle while your account quietly whispers, “That was never my job.”

In this Empower Personal Cash review, we will break down what the account does well, where it falls short, who should consider it, and who should probably keep shopping. The short version: it is a strong option for savers who want yield, flexibility, and a clean connection to the broader Empower dashboard, but it is not the best pick for people who need a daily spending account with every checking feature under the sun.

What Is Empower Personal Cash?

Empower Personal Cash is a cash management account, or CMA. That means it blends some features of checking and savings into one place. Instead of acting like a traditional bank account with branches and tellers, it is built more like a digital cash hub. You can move money in and out, set up direct deposit, pay bills using your account and routing numbers, and earn interest on your balance.

What makes it different from a basic savings account is the way it fits into Empower’s broader money-management ecosystem. Empower is best known for its dashboard tools, net worth tracking, retirement planning features, and advisory business. So this account is not just a parking lot for cash. It is also part of a larger financial picture. If you already use Empower to track your spending, investments, and long-term goals, Personal Cash can feel like a natural extension rather than a random extra tab.

The account is offered with UMB Bank and a network of program banks, which is how Empower can provide more FDIC insurance than a standard single-bank account. That sounds fancy, but the basic idea is simple: your money can be spread across participating banks so more of it can stay insured.

Quick Verdict

Empower Personal Cash is best for people who want a no-fee place to hold cash, earn a competitive yield, and see that cash alongside the rest of their financial life inside one dashboard. It is especially appealing for people who like automation, linked accounts, and a big-picture money view.

It is less ideal for people who want a true everyday checking account. There is no debit card. There is no checkbook. That means the account behaves more like a modern cash reserve with transfer tools than a replacement for the account you use to buy coffee, split dinner, or panic-order batteries at 11:47 p.m.

What Empower Personal Cash Does Well

No Monthly Fees and No Minimum Balance

This is one of the account’s strongest selling points. Empower Personal Cash does not hit you with a monthly maintenance fee, and it does not require a minimum daily balance to keep the account open. That makes it accessible for people who are just building savings and useful for people who do not want to babysit their balance to avoid penalties.

That also makes the account psychologically easier to use. There is something refreshing about a financial product that does not act like it is doing you a favor just by existing. You can park a smaller emergency fund here, build a house down payment stash, or keep a larger cash cushion without worrying that the account will punish you for being too rich, too broke, or too human.

High FDIC Coverage Is a Real Advantage

One of the biggest reasons people notice Empower Personal Cash is the FDIC coverage. Through UMB Bank and participating program banks, Empower advertises aggregate coverage up to $5 million for individual accounts, and up to $10 million for joint accounts. For savers with larger balances, that is a meaningful feature.

Why does that matter? Because a standard deposit account at a single bank is usually insured up to $250,000 per depositor, per ownership category, per insured bank. Once you start holding more cash than that, you need to think about how your money is structured across institutions. Empower simplifies part of that process by using multiple program banks. In plain English, it can save higher-balance savers from having to play a manual shell game with several bank logins.

That said, there is an important catch: if you already hold deposits at one of the program banks, those balances may count toward your insurance limit at that bank. So the headline number is impressive, but smart savers should still read the details instead of high-fiving the screen and moving on.

Strong Fit for the Empower Dashboard

This may be the most underrated benefit of the account. Empower’s biggest strength has long been financial visibility. The platform gives users a consolidated view of spending, net worth, debts, investments, and cash flow. Personal Cash fits neatly into that structure. Instead of using one app for budgeting, another for banking, and a third for long-term planning, you can bring more of your financial life into one place.

That is not just convenient. It can actually improve behavior. People tend to make better money decisions when they can see the full picture. A high-yield cash account sitting next to your monthly spending, investment balances, and future goals can make it easier to decide whether that money is truly “extra” or whether it already has a job.

Useful Cash Movement Features

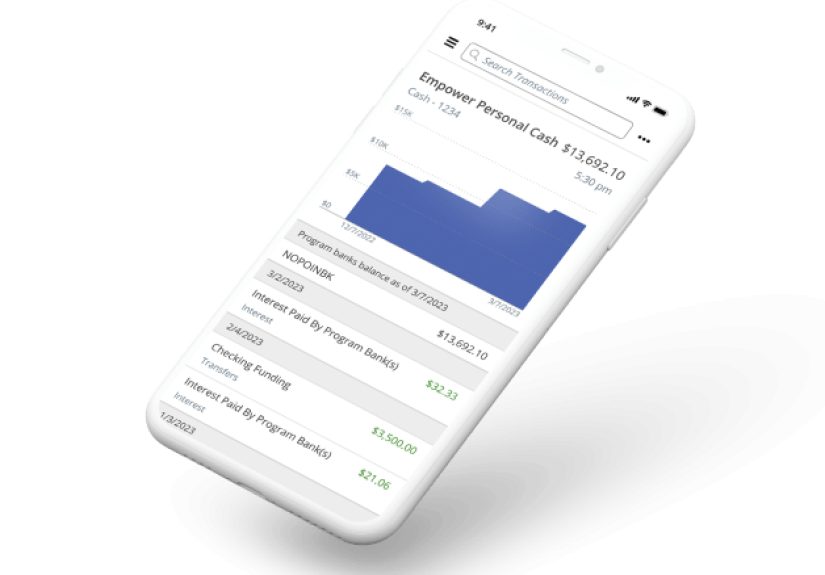

Empower Personal Cash supports ACH transfers, direct deposit, bill payments through account and routing numbers, and even wire transfers in certain situations. Interest accrues daily and is paid monthly, which is what most savers want to see from a serious cash account.

There are also recurring transfer options, which can be excellent for building savings on autopilot. If you are the kind of person who says, “I’ll save what’s left at the end of the month,” this account can help you upgrade to the smarter version: “I saved first, so there wasn’t much left to accidentally spend.”

Where Empower Personal Cash Falls Short

No Debit Card and No Paper Checks

This is the deal-breaker for some people, and it should not be glossed over. Empower Personal Cash does not come with a debit card or checkbook. That immediately limits its usefulness as a primary checking account.

Yes, you can still pay bills and move money around. But there is a difference between “I can pay my mortgage through account details” and “I can use this as my everyday spending account.” If you want ATM access, point-of-sale purchases, and the kind of flexible spending tools many people expect from a checking account, Empower Personal Cash is simply not built for that lane.

Transfer Speeds Matter More Than the Marketing

Cash management accounts often sound like they can do everything, but real life happens in timeframes, not taglines. Empower’s support materials note that deposits may take a few business days before they are available for withdrawal, and outbound withdrawals generally are not instant either. That is normal for many digital cash products, but it means this should not be your only source of immediate money access.

If your emergency fund is here, great. Just make sure your “today money” lives somewhere else. In other words, this is a smart place for reserve cash, not the account you want to rely on when the dog eats a sock and the vet wants payment immediately.

APY Is Competitive, but It Is Also a Moving Target

Empower Personal Cash has offered a competitive APY relative to many traditional banks, but the exact number has shifted over time as interest rates changed. Recent official disclosures showed separate standard and premium APY tiers, with the premium rate tied to qualifying recurring deposits. Third-party reviewers also captured higher yields at earlier points in the rate cycle.

The lesson here is simple: do not fall in love with any screenshot. Yield is one of the account’s strengths, but it is variable. That does not make the account bad. It just means your decision should be based on the structure of the account and not only on one rate quote that may age like a banana on a dashboard.

How Empower Personal Cash Compares to a High-Yield Savings Account

If you are comparing Empower Personal Cash with a plain high-yield savings account, the biggest difference is flexibility. Empower offers more money-movement functionality and tighter integration with personal finance tools. A basic high-yield savings account may be simpler, but it usually does less.

On the other hand, some online savings accounts and competing CMAs offer more checking-style perks, such as debit access, ATM networks, or a more mature day-to-day banking experience. Empower does not really try to win that contest. Its value proposition is different. It is saying, “Put your cash here, earn a good yield, move money when needed, and keep everything visible in one place.” That pitch will land well with some users and fall flat with others.

Who Should Open Empower Personal Cash?

This account makes the most sense for a few specific types of users. First, it is a good fit for people who already use Empower’s dashboard and want a dedicated cash account inside the same ecosystem. Second, it works well for savers who keep a meaningful amount of idle cash and want better insurance structuring than a standard single-bank setup. Third, it is useful for goal-based savers who want to automate deposits and keep cash separate from spending temptation.

It is also attractive for people who appreciate a cleaner digital setup. If you like seeing your emergency fund, bills, investments, and net worth in one financial command center, Empower Personal Cash is more compelling than it might look on paper.

Who Should Probably Pass?

You should probably skip this account if you want one account to handle all your daily spending needs. No debit card and no checks will be a hard stop for some households. You may also want a different account if instant cash access is crucial, if you frequently need ATM withdrawals, or if you prefer a straightforward bank experience over an ecosystem-driven one.

It may also be a mismatch for people who do not care about financial dashboards and simply want the absolute highest rate in the market at any given moment. Empower’s appeal is the combination of yield, usability, and integration. If you only care about squeezing out every last basis point, you will probably keep rate-shopping anyway.

My Take on the Real User Experience

The most honest way to describe Empower Personal Cash is this: it feels less like a checking account and more like a very organized holding area for smart money. It is the account for cash that has a purpose but does not need to be touched every hour. Think emergency fund, tax reserve, home repair fund, future travel money, or the chunk of your paycheck that you want to protect from your own “just browsing” behavior.

Using it likely feels best when it is paired with another account. Your main checking account handles groceries, subscriptions, and everyday chaos. Empower Personal Cash handles the calm, strategic side of your money life. That division of labor makes the product more appealing and prevents disappointment. When used that way, the account’s limitations stop feeling like flaws and start feeling like boundaries.

I also think the Empower dashboard gives this account an edge that is easy to underestimate. Plenty of cash products can hold money. Fewer can help you understand how that money fits into the rest of your life. If the goal is not just earning yield but also improving financial awareness, Empower has a stronger argument than many bare-bones competitors.

Experience-Based Scenarios: What It Feels Like in Real Life

Imagine a user named Maya who keeps $20,000 in a sleepy brick-and-mortar savings account because that is where it has always been. She is not reckless with money. She just has not revisited the setup in years. When she moves that balance into a cash management account like Empower Personal Cash, the first noticeable difference is not dramatic fireworks. It is clarity. She can see the account next to her credit cards, mortgage, retirement accounts, and monthly cash flow. Suddenly, her emergency fund stops feeling like random money in a hidden drawer and starts feeling like an intentional part of a larger plan.

Now picture Daniel, who is self-employed and likes keeping a tax reserve separate from his everyday spending money. He does not need a debit card for that reserve. In fact, he would rather not have one. Friction is helpful when the money has a job. For someone like Daniel, Empower Personal Cash can feel like a smart buffer zone. He can automate transfers, earn interest while the cash sits there, and avoid mixing business obligations with weekend spending decisions that begin with “I deserve a treat” and end with a suspicious number of online receipts.

Then there is the household that already uses Empower’s dashboard to track everything. For that user, opening Personal Cash may feel less like adding another account and more like finishing a puzzle. The budget tools, net worth view, retirement estimates, and linked balances all begin to work together more naturally. That kind of cohesion has value. It reduces the mental clutter that comes from juggling multiple apps, multiple institutions, and multiple half-finished ideas about where money is supposed to live.

Of course, the real-life experience is not perfect for everyone. A user trying to make Empower Personal Cash their one and only spending account may quickly run into frustration. No debit card means no casual tap-to-pay life. No checkbook means some older-school payment habits need to shift. Transfer timing also reminds you that this account is built for organized cash, not instant-gratification cash. If you expect it to behave exactly like a primary checking account, the experience can feel like bringing a tennis racket to a soccer game. Nice equipment, wrong sport.

But when expectations match the product, the experience is much better. The ideal user does not open Empower Personal Cash to replace every financial tool. They open it to give their cash a smarter home. They want yield, visibility, automation, and structure. They want an account that quietly does its job while the rest of their financial picture becomes easier to understand. In that role, Empower Personal Cash can feel less like a flashy fintech experiment and more like a practical upgrade for grown-up money management.

Final Verdict

Empower Personal Cash is a strong cash management account for the right user. It shines with no monthly fees, no minimum balance requirement, high aggregate FDIC coverage, and solid integration with Empower’s broader financial tools. For people who want a cash reserve account that works alongside budgeting, planning, and net worth tracking, it is a compelling option.

Its weaknesses are equally clear. This is not a full-featured checking account. No debit card and no paper checks will matter to plenty of people. Transfer timing may also make it a poor fit for anyone who wants instant everyday access. So the account is not trying to be everything. It is trying to be a smart place for meaningful cash balances. In that role, it succeeds more often than it stumbles.

Bottom line: if you want a high-yield cash hub inside a polished financial dashboard, Empower Personal Cash deserves a serious look. If you want your next account to replace your wallet, your ATM card, and your old checking habits all at once, keep browsing.