Table of Contents >> Show >> Hide

- First Things First: What Is the Fed Actually Doing?

- Why Rate Hikes Make Investors Nervous

- What Happens to Stocks When the Fed Raises Rates?

- What Happens to Bonds When the Fed Raises Rates?

- What History Says: It’s Not All Doom and Gloom

- How to Invest When the Fed Is Raising Rates

- The “A Wealth of Common Sense” Takeaway

- Real-World Experiences When the Fed Raises Rates

- Bottom Line: Rate Hikes Aren’t the End of the World

Few four-word phrases spook investors as quickly as “The Fed raised rates.”

Suddenly every red blip on your brokerage app feels like the beginning of the end,

and that calm, long-term investor you were yesterday is now refreshing market news every 30 seconds.

But here’s the thing: history is a lot less dramatic than the headlines.

Rate hikes don’t automatically “kill” stocks or bonds, and the story is far more nuanced than

“higher rates = everything crashes.” A common-sense approach inspired by the perspective of

Ben Carlson’s A Wealth of Common Sense shows that markets often behave in surprisingly

normal, even boring, ways when the Federal Reserve starts nudging interest rates higher.

Let’s break down what’s really going on with stocks and bonds when the Fed raises rates,

how it has played out historically, and what it means for your portfolio today.

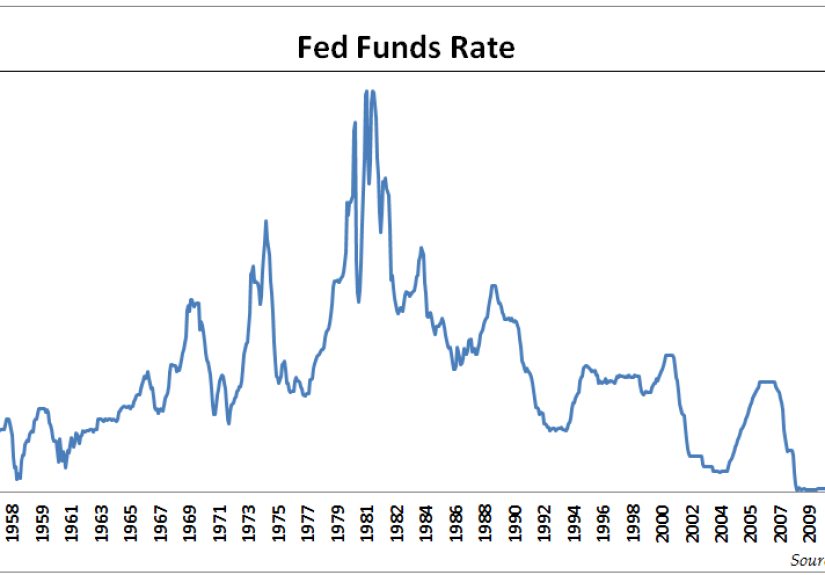

First Things First: What Is the Fed Actually Doing?

When people say “the Fed is raising rates,” they’re talking about the federal funds rate

the short-term interest rate banks charge each other for overnight loans.

The Fed doesn’t directly set mortgage rates, credit card rates, or bond yields,

but its policy rate heavily influences them over time.

Why raise rates at all? Usually to:

- Cool down inflation when the economy is running too hot.

- Prevent asset bubbles by making borrowing less ridiculously cheap.

- Normalize policy after periods of ultra-low rates (like after recessions or crises).

The key point: the Fed is not targeting your portfolio personally.

It’s trying to balance inflation and growth in the overall economy.

Markets then react sometimes rationally, sometimes emotionally to what that means

for corporate earnings, borrowing costs, and future returns.

Why Rate Hikes Make Investors Nervous

Higher rates ripple through the economy:

- Borrowing gets more expensive for businesses and consumers.

- Corporate profits may face pressure as interest costs rise.

- Spending and investment can slow, especially in rate-sensitive areas like housing and autos.

- “Safer” assets like cash and short-term bonds become more attractive relative to risky stocks.

In theory, this should hurt stock prices and existing bonds. In practice, the story is messier.

Markets don’t react to what’s happening today as much as they react to

whether reality is better or worse than expected.

If the Fed hikes but investors already saw it coming, the market might shrug.

If the Fed surprises everyone, then you see fireworks.

What Happens to Stocks When the Fed Raises Rates?

Short-Term: Volatility, Headlines, and Overreactions

The first thing you’ll usually notice when the Fed hikes is noise:

- Intraday swings as traders react to every line of the Fed statement.

- Financial TV trying to interpret every adjective from the Fed chair’s press conference.

- Social media declaring either “endless bull market” or “this is it, we’re doomed.”

Historically, the average one-day move in the S&P 500 on a Fed hike day has been pretty modest.

Over the weeks that follow, returns are mixed sometimes positive, sometimes negative

but there’s no consistent pattern of stocks collapsing just because rates ticked up.

Medium-Term: Earnings vs. Valuations

Over the next 6–24 months, two forces battle it out:

-

Corporate earnings: If the Fed is hiking because the economy is strong,

companies may still grow profits even with higher borrowing costs. -

Valuation pressure: Higher interest rates raise the “discount rate” used to value future cash flows,

which tends to hit high-growth, high-multiple stocks the hardest.

Historically, stocks have often delivered positive returns during rate hike cycles,

especially when hikes start from very low levels and the economy is healthy.

The problem isn’t “rates are rising;” the problem is usually “rates rose a lot,

the economy slowed, or inflation stayed sticky.”

Different Sectors React Differently

Not all stocks carry the same interest-rate baggage. In a rising-rate environment, you often see:

-

Financials sometimes benefit if higher rates improve net interest margins

(though an overly flat or inverted yield curve can spoil that). -

Utilities and REITs can struggle, because they trade a bit like “bond proxies”

and their dividends compete with higher bond yields. -

High-growth tech or speculative names may feel the pressure as investors become less willing

to pay rich valuations when “risk-free” yields are higher. -

Value and dividend stocks can sometimes hold up better, especially if their earnings

are tied to solid, cash-generating businesses.

Again, none of this is guaranteed. The market is not a vending machine where you insert a 0.25% hike

and get a pre-labeled outcome.

What Happens to Bonds When the Fed Raises Rates?

The Big Rule: Bond Prices and Yields Move in Opposite Directions

With bonds, the basic rule is simple enough to write on a sticky note:

when interest rates rise, bond prices fall.

New bonds come out with higher yields, so investors demand a discount on older bonds with lower coupons.

That’s why rising-rate environments can feel painful for bond investors.

Bond mutual funds and ETFs mark their holdings to market every day,

so you see those price drops in your account even if you haven’t sold anything.

Duration: How Sensitive Is Your Bond to Rate Changes?

Not all bonds react equally. The key concept is duration a measure, in years,

of how sensitive a bond (or bond fund) is to changes in interest rates.

-

Short-duration bonds (like 1–3 year Treasuries) usually see

small price moves when rates change. -

Intermediate-term bonds balance income and volatility,

making them a popular “core” fixed-income holding. -

Long-duration bonds (20–30 years) can swing dramatically.

They’re great when rates fall, brutal when rates rise.

For example, if a bond fund has a duration of 6, a 1% rise in rates might translate,

very roughly, into about a 6% drop in price at least in the short run.

The flip side is that over time, the fund reinvests at higher yields,

which can help long-term investors recover and even come out ahead.

Individual Bonds vs. Bond Funds

The experience of rising rates looks different depending on how you own bonds:

-

Individual bonds: If you hold to maturity and there’s no default,

you get your principal back and collect coupons along the way.

Market price fluctuations in between are mostly “paper noise.” -

Bond funds and ETFs: There’s no maturity date.

The fund continually reinvests, so your account value moves daily with prices and yields.

Short-term losses from price drops may be offset over time by higher income.

Rising rates hurt your bond statement in the near term

but they also lay the groundwork for better future returns

because new bonds pay more income.

What History Says: It’s Not All Doom and Gloom

When you look back at past Fed hiking cycles, a couple of themes stand out:

-

Stocks often survive and sometimes thrive during rate hikes.

As long as the economy is expanding and earnings are growing, stocks can deliver positive returns even

while the Fed is tightening. -

Bonds may struggle at first but improve over time.

Initial price drops may sting, but higher ongoing yields can make long-term bond returns more attractive. -

Expectations matter more than the hike itself.

Markets tend to price in Fed moves well in advance.

Surprises not routine, well-telegraphed hikes are what usually cause bigger dislocations.

The historical record backs up the idea that

“stocks and bonds both getting completely destroyed the moment the Fed hikes” is more myth than law.

Outcomes depend on where inflation is, how strong the economy is,

and whether investors are blindsided or already prepared.

How to Invest When the Fed Is Raising Rates

1. Avoid All-or-Nothing Moves

Panic moves going 100% to cash, dumping every bond,

or betting the farm on whatever did well last week rarely age well.

Rate hikes are just one piece of a very large macro puzzle.

2. Revisit Your Time Horizon

Your time horizon matters far more than the next Fed meeting:

-

If you’re investing for decades, short-term rate moves are background noise.

Stocks will live through many cycles. -

If you need money in the next 1–3 years,

you should already be relying more on cash, short-term bonds, and stable reserves anyway.

3. Make Your Bonds Work Smarter

In a rising-rate environment, you might:

- Tilt toward short- and intermediate-term bonds to reduce interest rate risk.

- Consider a bond ladder staggering maturities so you can reinvest steadily at higher yields.

-

Focus on high-quality issuers so you’re not taking unnecessary credit risk

on top of rate risk.

4. Keep Perspective with Stocks

Rather than obsessing over the Fed, it’s often more useful to focus on:

- Whether your portfolio is diversified across sectors and styles.

- Whether you’re paying reasonable valuations, especially for growth stocks.

- Whether your stock allocation matches your risk tolerance and time horizon.

The Fed may drive the daily headlines, but long-term returns usually follow

earnings growth, cash flows, and staying invested through cycles.

The “A Wealth of Common Sense” Takeaway

The spirit of A Wealth of Common Sense is pretty straightforward:

markets are complicated, investors are emotional, and rules-of-thumb like

“rates up, everything down” are dangerously oversimplified.

History shows that:

- Stocks don’t automatically collapse when the Fed hikes.

- Bonds may deliver disappointing returns for a while then benefit from higher yields.

- Trying to time every Fed move is usually less effective than following a disciplined plan.

Instead of obsessing over each quarter-point move,

focus on what you can actually control: your savings rate, asset allocation, costs, and behavior.

The Fed will do what it needs to do. You should, too.

Real-World Experiences When the Fed Raises Rates

It’s one thing to understand the theory. It’s another to live through a rate-hiking cycle with real money on the line.

Let’s look at how different types of investors typically experience Fed hikes and what they often learn the hard way.

The “All-In on Growth Stocks” Investor

Imagine an investor who loaded up on high-flying growth stocks when rates were near zero.

These companies looked unstoppable: rapid revenue growth, flashy narratives, sky-high valuations.

When the Fed starts raising rates, this investor doesn’t feel the pain instantly

but as the hikes accumulate and bond yields climb, the market starts asking harder questions about

how much to pay for distant profits.

Suddenly, that basket of growth names is down 30–50%, even though the underlying businesses are still growing.

The big lesson here isn’t “never buy growth.” It’s that valuation and interest rates are joined at the hip.

When the “risk-free” rate was barely above zero, investors were willing to pay almost anything for potential.

Once rates rose, that math changed, and so did sentiment.

The “Bonds Are Always Safe” Investor

Another investor thought of bonds as the sleepy, no-drama corner of their portfolio.

They chose a long-term bond fund because the yield looked a little higher,

assuming “it’s still fixed income, how risky can it be?”

When the Fed pushed rates higher, long-term yields jumped and the prices of those bonds sank.

On paper, the fund’s value slid more than expected enough to cause a mild panic.

It felt like bonds had “failed.”

But over the next few years, as those bonds matured or were replaced,

the fund began reinvesting into much higher yields.

The short-term mark-to-market loss set the stage for stronger future income.

The experience taught this investor the importance of:

- Understanding duration before chasing yield.

- Owning bonds for stability and income over a full cycle, not just one year.

- Separating short-term price swings from long-term purpose.

The “Cash on the Sidelines” Investor

Then there’s the investor who sat in cash for years, worried that the next Fed hike,

or the next headline, would be the one that finally breaks the market.

They waited for the “perfect entry point” that never quite arrived.

During this time, stocks went through corrections and recoveries,

while bond yields slowly reset higher.

Yes, they avoided some volatility, but they also missed years of compounding.

The painful realization? The risk of never investing can be just as real as

the risk of investing before a rate hike.

Their big takeaway: build a rules-based plan such as dollar-cost averaging

instead of trying to outsmart every Fed decision.

The Balanced, Boring Investor

Finally, consider the investor who:

- Holds a diversified mix of stocks and bonds.

- Uses intermediate-term, high-quality fixed income as ballast.

- Rebalances periodically instead of reacting emotionally.

For this person, Fed rate hikes register mostly as background noise.

Some years the stock side struggles. Some years bonds disappoint.

But over time, the combination of diversification, higher bond income after hikes,

and staying invested tends to produce steady progress.

Their experience reinforces the central, common-sense lesson:

it’s your behavior, not the Fed, that usually makes or breaks your results.

Bottom Line: Rate Hikes Aren’t the End of the World

When the Fed raises rates, both stocks and bonds feel the impact but not in a simple, one-directional way.

Stocks may wobble as valuations adjust and growth expectations get recalibrated.

Bonds may suffer near-term price drops even as their future income improves.

History suggests that neither asset class is automatically doomed by higher rates.

Instead of reacting to every move from the Fed, smart investors:

- Keep a long-term perspective.

- Use diversification and sensible bond strategies.

- Focus on earnings, cash flow, and fundamentals not just policy headlines.

- Stick to a plan that fits their goals, not the news cycle.

Interest rates will rise and fall many times over your investing lifetime.

Your best edge isn’t predicting those cycles it’s building a portfolio and mindset

resilient enough to live through them.