Table of Contents >> Show >> Hide

- Default vs. Delinquency: The “Late” Phase Comes First

- The First Wave: Fees, Interest, and the “Ugh” Charges

- Acceleration: When “Catch Up” Becomes “Pay It All”

- Credit Damage: The Part That Lingers Like a Bad Smell

- Collections: Calls, Letters, and Your Rights

- Lawsuits, Judgments, and Garnishment: When Paper Turns Into Court Paper

- Secured Loans: When the Lender Can Take Something Back

- Federal Student Loans: Default Has Extra “Government Powers”

- Surprise Twist: Default Can Create a Tax Problem

- How to Limit the Damage (Even If You’re Already in Trouble)

- How to Avoid Default in the First Place (Without Becoming a Spreadsheet Monk)

- Final Thoughts

- Real-World Experiences People Often Describe After a Loan Default (About )

- Experience #1: The Personal Loan That Turned Into a Calendar of Anxiety

- Experience #2: The Car Repossession That Didn’t End When the Car Left

- Experience #3: Mortgage Trouble and the Moment “Loss Mitigation” Became a Lifeline

- Experience #4: Student Loan Default and the Wake-Up Call of Involuntary Collections

Defaulting on a loan is a little like ignoring a “check engine” light: the car might keep running for a bit, but the longer you pretend you didn’t see it, the more expensive (and dramatic) the ending gets.

In real life, a loan default can trigger fees, credit damage, aggressive collection attempts, anddepending on the type of loanrepossession, foreclosure, lawsuits, or government collections.

The exact timeline varies by lender, contract, and state rules, but the “domino order” is surprisingly consistent.

This guide breaks down what a loan default usually means in the U.S., what steps lenders and collectors typically take, how your credit report gets involved, and what you can do to limit the fallout (and get your life back from your inbox).

It’s educationalnot legal advicebut it will help you walk into the situation with your eyes open and your panic level turned down.

Default vs. Delinquency: The “Late” Phase Comes First

Most people use “default” as shorthand for “I missed a payment,” but lenders usually separate the world into phases:

current, delinquent, and default.

Delinquency: You’re late, and the clock is running

If you miss a due date, you’re typically delinquent right away. That can trigger late fees and extra interest.

Many lenders report a missed payment to the credit bureaus once you’re 30 days past due (some do it later, but 30 days is the common marker).

A key exception: federal student loan delinquency is generally reported after 90 days.

Default: The lender says, “We’re done playing nice”

“Default” usually means you’ve been delinquent long enough that the lender can use stronger remedies under your contractlike sending you to collections, accelerating the debt (making the full balance due), or taking collateral.

For many consumer loans, default often happens somewhere around the 120–180 day range of nonpayment, but your loan agreement controls the definition.

The First Wave: Fees, Interest, and the “Ugh” Charges

Before the big scary stuff, most defaults start with smaller, painful paper cuts:

- Late fees: Often a flat fee or percentage (check your promissory note).

- Penalty interest or default interest: Some contracts allow a higher rate once you’re past due.

- Collection costs: If the account is placed with a collector or attorney, additional costs may be added where allowed by contract and law.

- Returned payment fees: If a payment bounces, that’s another fee waiting in the wings.

The frustrating part is that these charges don’t just make you feel worsethey can make it harder to catch up because your “past due” amount grows faster than your motivation.

Acceleration: When “Catch Up” Becomes “Pay It All”

Many loan contracts include an acceleration clause. That means if you default, the lender can declare the entire remaining balance immediately duenot just the missed payments.

Even if you’re thinking, “I can catch up next month,” acceleration can change the conversation to, “Great! Please send the full amount by Tuesday.”

Acceleration is especially common in secured lending (like mortgages and auto loans), and it’s one reason people feel like the situation escalated “overnight.”

It didn’tthere was just a clause quietly doing push-ups in the corner.

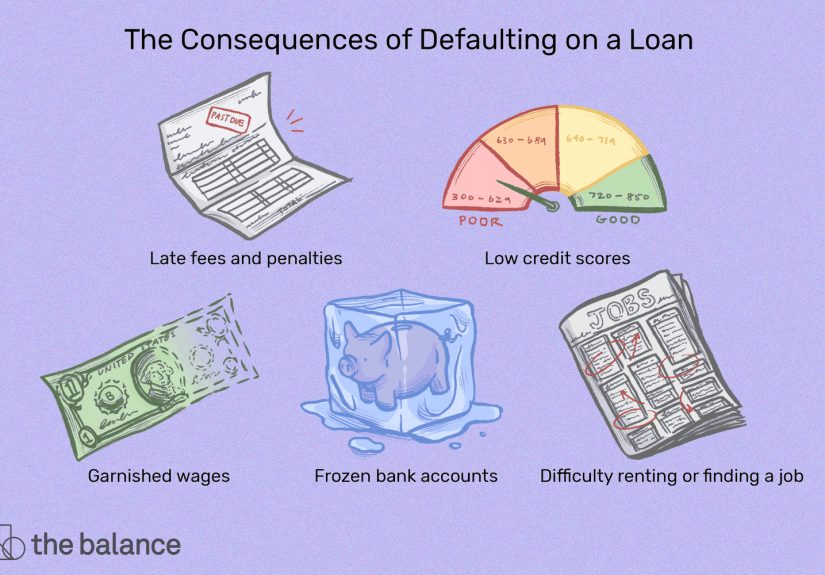

Credit Damage: The Part That Lingers Like a Bad Smell

Credit scores are basically risk forecasts, and default is the credit-scoring equivalent of telling the weather app, “Yes, it is currently raining inside my house.”

Here’s how the credit impact typically unfolds:

Late payments get reported first

Once a lender reports you as 30 days late (or 60/90/120 days late), that negative history can lower your scoresometimes sharply, especially if you previously had strong credit.

And yes, the “payment history” category is a big deal in most scoring models.

Charge-off: The accounting move that does NOT erase the debt

If nonpayment continues, a lender may “charge off” the debtan accounting step where they treat it as a likely loss.

Important: a charge-off is not forgiveness. You can still owe the balance, and collection can continue (either by the original lender or a debt buyer).

Collections: A second negative mark may appear

If the debt goes to a collection agency or is sold to a debt buyer, you may see a collection account on your credit reports in addition to the original tradeline.

That can further damage credit and make future borrowing (and sometimes renting) more difficult.

How long does it stay on your credit report?

In general, most negative informationlike delinquencies, charge-offs, and collectionscan be reported for about seven years, typically tied to the original delinquency that led to the default.

Bankruptcies can remain longer (often up to ten years, depending on type).

Collections: Calls, Letters, and Your Rights

Once a loan is in collections, communication ramps up. You may get phone calls, letters, emails, and offers that sound like:

“We can settle today if you just sell one kidney and your favorite hoodie.”

(Do not sell kidneys. Also, collectors can’t legally suggest that. If they do, document it.)

Debt validation: the “prove it” moment

Under federal rules, debt collectors must provide certain information about the debt and your rights to dispute it.

If you think the amount is wrongor the debt isn’t yoursrequest validation and keep everything in writing.

Credit reporting by collectors

Collectors can report debts to credit reporting agencies, but they must follow specific steps and comply with credit reporting laws.

Bottom line: if the debt is being furnished to credit bureaus inaccurately, you have the right to dispute it with the bureaus (and, often, with the furnisher).

Lawsuits, Judgments, and Garnishment: When Paper Turns Into Court Paper

If you don’t resolve the default, the lender or debt collector may sue youespecially for larger balances.

A lawsuit can lead to a judgment, and a judgment can unlock stronger collection tools, depending on your state:

- Wage garnishment: A portion of your paycheck can be taken (limits and rules vary).

- Bank account levy: Funds in a bank account may be seized (state exemptions may protect some funds).

- Liens: A legal claim against property may be filed in some cases.

A key “it depends” detail: statutes of limitations for debt lawsuits vary by state and by debt type. Even if a collector can’t sue (because the limitation period has passed), they may still attempt to collect.

If you’re being threatened with a lawsuit, it can be worth talking to a consumer law attorney in your statebecause the rules change at the border like accents and barbecue styles.

Secured Loans: When the Lender Can Take Something Back

Secured loans are backed by collaterallike a car or a homeso default can involve losing the thing you borrowed against.

Auto loans: repossession and deficiency balances

If you default on an auto loan, the lender may have the right to repossess the vehicle.

In many states, repossession can happen without going to court, as long as it’s done without “breach of the peace.”

After repossession, the car is usually sold (often at auction).

Here’s the part people don’t expect: if the sale price doesn’t cover what you owe plus repossession and sale fees, you can still owe the remaindercalled a deficiency balance.

If the car sells for more than the payoff and allowed costs, you may be entitled to a surplus.

Mortgages: loss mitigation, foreclosure timelines, and real consequences

Mortgage default is its own universe because it involves your home, federal servicing rules, and state foreclosure procedures.

If you can’t pay your mortgage, the best move is usually to contact your servicer immediately and ask about loss mitigationoptions like repayment plans, modifications, or forbearance.

Federal mortgage servicing rules generally provide important protections early in delinquency, and servicers must follow procedures when you apply for help.

Foreclosure timelines vary by state, but the key theme is: the sooner you apply for assistance, the more options you tend to keep on the table.

Federal Student Loans: Default Has Extra “Government Powers”

Federal student loans have a set of consequences that can be more intense than typical consumer debtbecause the federal government has collection tools that don’t always require a traditional lawsuit first.

If you default on a federal student loan, you may face:

- Acceleration: the full balance can become due immediately.

- Collection costs: added fees can increase what you owe.

- Administrative wage garnishment: wages may be garnished under federal processes.

- Treasury offset: tax refunds and certain federal payments can be intercepted.

- Credit reporting damage: delinquency and default can appear on credit reports.

The good news (yes, there is some): there are established pathways to get out of default, including rehabilitation and consolidation (eligibility rules apply).

If you’re in this situation, it’s usually better to engage early than to attempt the “I simply will become a forest hermit” strategy.

Surprise Twist: Default Can Create a Tax Problem

Sometimes, after months or years, a creditor agrees to settle for less than you oweor cancels the debt.

If a lender cancels or forgives $600 or more, they may issue a Form 1099-C, and the IRS generally treats canceled debt as taxable income unless an exception applies.

Common exceptions can include bankruptcy discharges and certain situations of insolvency, among others.

Translation: if you settle a debt, you might save moneyand then owe taxes.

It’s the financial version of “You won!” followed by “Also, here’s your bill.”

How to Limit the Damage (Even If You’re Already in Trouble)

If you’re heading toward defaultor already therethe goal is to stop the situation from getting more expensive and more permanent than it needs to be.

A few moves tend to help across most loan types:

1) Contact the lender or servicer early

Ask about hardship options: due date changes, temporary forbearance, reduced payment plans, or modifications.

You don’t need a perfect speech. A simple “I’m having trouble; what options do you have?” is enough to start.

2) Get everything in writing

If someone offers a plan, request the terms in writing. Save emails, letters, and screenshots.

Keep a log of calls (date, time, name, what was said).

Future-you will be grateful.

3) Prioritize secured debts if you’re trying to protect essentials

If you’re choosing what to pay with limited money, losing a car or housing can be life-altering.

That doesn’t mean unsecured debt doesn’t matterit doesbut the consequences of secured debt default can hit faster and harder.

4) Consider nonprofit credit counseling

Legitimate nonprofit credit counselors can help you build a plan, negotiate a debt management arrangement for certain debts, and avoid scams that promise miracle deletions from your credit report.

If someone guarantees they can erase accurate negative marks from your credit history, treat that like a “free vacation” text from a random number.

5) Dispute errors the right way

If your credit report shows incorrect dates, wrong balances, or accounts that aren’t yours, dispute with the credit bureaus and the furnisher.

Accurate information generally stays; inaccurate information should be corrected.

How to Avoid Default in the First Place (Without Becoming a Spreadsheet Monk)

- Set up autopay for at least the minimum payment (and keep a buffer in the account).

- Use due-date alignment: move due dates near your payday if your lender allows it.

- Build a “one payment” emergency buffer: even a small cushion can prevent a cascade.

- Act at the first missed payment: the earlier you engage, the more options you usually have.

- Know your loan terms: especially default triggers, fees, and whether the loan is secured.

Final Thoughts

Defaulting on a loan is seriousbut it’s not the end of your financial life.

The consequences tend to follow a predictable pattern: delinquency, fees, credit reporting, collections, and then (for some loans) repossession, foreclosure, lawsuits, or government collection actions.

The faster you respond, the more control you tend to keep.

If you’re staring at missed payments right now, your best “first win” is simply this: open the mail, answer the calls you can verify, and start negotiating from a position of information instead of fear.

The goal isn’t perfectionit’s preventing the situation from snowballing into a boulder.

Real-World Experiences People Often Describe After a Loan Default (About )

The stories below are composite examplesnot one specific person’s lifebuilt from common patterns borrowers report when a loan goes from “late” to “default.”

If you’re in this position, you’ll probably recognize at least one of these feelings: embarrassment, confusion, and a weird amount of adrenaline every time your phone buzzes.

Experience #1: The Personal Loan That Turned Into a Calendar of Anxiety

A borrower misses one personal loan payment after a medical expense and tells themselves it’s a one-time slip. The next month is tight again, so they skip “just this once” again.

By the time they’re 60 days late, the lender’s tone has changed: late fees stack up, the past-due amount is bigger than expected, and the borrower starts avoiding the lender’s calls.

Avoidance feels good for about three minutesright until the email arrives that mentions “collections” and “possible legal remedies.”

The borrower eventually calls, finds out there was a temporary hardship plan, and realizes (with equal parts relief and frustration) that earlier contact would have reduced fees and stress.

The big lesson they take away: silence is expensive.

Experience #2: The Car Repossession That Didn’t End When the Car Left

Another borrower falls behind on a car payment during a job transition. They assume repossession is a slow process with lots of warnings.

Instead, one morning the car is gone. The borrower feels shocked and angry, then embarrassed, then furious againsometimes all before lunch.

They learn the car was sold, but the sale price didn’t cover the loan balance and costs. Now there’s a deficiency balance.

The borrower tries to negotiate the deficiency and learns the importance of getting everything in writing and asking for a breakdown of fees.

The most surprising part? The emotional whiplash of losing transportation while still owing money for the thing they can’t drive anymore.

Experience #3: Mortgage Trouble and the Moment “Loss Mitigation” Became a Lifeline

A homeowner starts missing mortgage payments after a reduction in household income.

At first, they’re sure they’ll catch upuntil the numbers prove otherwise.

When they finally contact the servicer, they learn there are options like forbearance or modification pathways, but the process requires paperwork, deadlines, and follow-through.

The homeowner describes the experience as “a part-time job made of PDFs,” but also notes that once they submitted a complete application, communication became clearer.

Even when the outcome isn’t perfect, engaging early often preserves choices and reduces the risk of a worst-case timeline.

Experience #4: Student Loan Default and the Wake-Up Call of Involuntary Collections

A former student ignores federal student loan notices for months, telling themselves they’ll deal with it after things calm down.

The problem is: things don’t calm down on a schedule.

Eventually, the borrower learns about consequences like tax refund offsets or wage garnishment processes.

That discovery creates an urgent pivot: they start exploring rehabilitation or consolidation to get the loan back into good standing.

The emotional takeaway is common: the borrower wishes they had asked for help sooner, but they also feel real hope once they see there’s an official path out of default.