Table of Contents >> Show >> Hide

- A 2026 Snapshot: Same Headache, Different Flavor

- The Biggest Difference: Mortgage Design Changes the Entire Game

- Supply Problems: One Shortage, Two Different Stories

- Price Trends: America Is Cooling; Australia Is Splitting

- Buying Culture: Negotiation vs. Auction Nerves

- Government Policy and Tax Incentives

- Which Market Is Tougher for First-Time Buyers?

- What Sellers and Investors Should Notice

- Real-World Experiences: What This Comparison Feels Like in Practice

- Conclusion

The U.S. and Australian housing markets speak the same language in one very important way: both can make perfectly rational adults stare at a mortgage calculator like it just insulted their family. But beyond that shared emotional damage, these two markets work in very different ways. The financing structure is different. The tax incentives are different. The buying culture is different. Even the way supply shortages show up feels different.

In 2026, both countries are still dealing with affordability strain, higher borrowing costs than buyers got used to during the pandemic boom, and a shortage of homes where people actually want to live. Still, the U.S. market looks more like a giant, uneven machine that is slowly regaining balance, while the Australian market often feels like a pressure cooker with better beaches.

This matters for buyers, sellers, renters, investors, and anyone trying to understand why a three-bedroom house in one country feels “expensive but maybe doable,” while in the other it feels like it was priced by a comedian with a dark sense of humor. Let’s break down what separates the U.S. housing market from the Australian housing market, where they overlap, and what real people are experiencing on the ground.

A 2026 Snapshot: Same Headache, Different Flavor

The U.S.: slow, expensive, but starting to breathe again

The American housing market in 2026 is still heavily shaped by mortgage rates. Existing-home sales remain subdued by historical standards, and affordability is still tight. Even so, inventory has been improving in many markets, price growth has cooled to a much gentler pace, and some buyers finally have room to negotiate without needing three backup offers, a handwritten love letter, and the emotional resilience of a Navy SEAL.

In plain English, the U.S. market is no longer acting like the frenzied free-for-all of 2021. It is slower. It is more selective. It is still expensive, but it is less chaotic. Buyers in some regions are seeing more homes on the market, more price cuts, and a little less of that “buy in seven minutes or lose forever” energy.

Australia: supply-starved, highly competitive, and still running hot

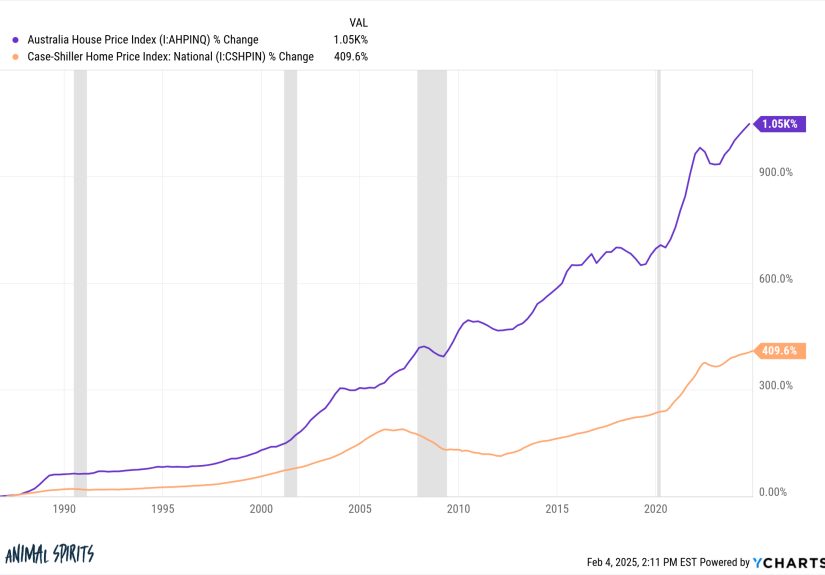

Australia’s housing market is also feeling the weight of interest rates and cost-of-living pressure, but national home values have remained remarkably resilient. Prices are still elevated, and in many areas they continue to rise. The country’s housing shortage, population growth, and chronic supply constraints keep feeding demand, especially in the more affordable or fast-growing cities.

That said, Australia is not one single market. Sydney and Melbourne can behave very differently from Perth, Brisbane, or Adelaide. Some cities are flattening or pulling back, while others are climbing at a speed that makes first-time buyers consider whether a stylish tent might count as “transitional architecture.”

The Biggest Difference: Mortgage Design Changes the Entire Game

If you want to understand why the U.S. and Australian housing markets feel so different, start with the mortgage.

In the U.S., the 30-year fixed-rate mortgage changes behavior

The American market is deeply shaped by the 30-year fixed-rate mortgage. That means many homeowners can lock in a rate and keep it for decades. When rates are low, owners become reluctant to sell because moving would mean giving up a cheap loan. This is one reason the U.S. has struggled with the “lock-in effect,” where homeowners stay put longer than they otherwise would.

The result is strange but powerful: even when buyer demand weakens, supply can stay tight because sellers do not want to trade a 3% mortgage for one above 6%. That helps explain why U.S. prices have not collapsed, even though affordability has taken a beating. The mortgage product itself acts like glue.

In Australia, variable rates and short fixed periods create faster pressure

Australia works differently. Variable-rate mortgages are much more common, and even fixed-rate loans are often fixed for a shorter term before resetting. That means interest-rate changes hit household budgets more directly and more quickly. When the Reserve Bank of Australia moves, many borrowers feel it sooner.

This makes the Australian market more sensitive to monthly repayment stress. Instead of millions of owners sitting comfortably on old, ultra-cheap 30-year loans, more households have to adjust as rates move. In theory, that should cool housing faster. In practice, limited supply and strong demand have often kept prices supported anyway.

Supply Problems: One Shortage, Two Different Stories

Both countries suffer from a housing supply problem, but the mechanics are not identical.

U.S. supply is improving, but not evenly

In the U.S., more inventory has been returning to the market in 2026. Some metro areas, especially where construction has been stronger, look noticeably more buyer-friendly than they did a year or two ago. Still, inventory is not back to what many economists would call normal, especially in high-demand neighborhoods and lower-priced starter-home segments.

Builders have helped, but the supply picture remains highly regional. A buyer in parts of Texas or the Southeast may feel the market softening. A buyer chasing a house in a top school district outside Boston or San Diego may laugh at the phrase “softening market” and then cry a little.

Australia’s shortage feels more structural

Australia’s supply challenge often looks more entrenched. New approvals can bounce from month to month, but the broad issue remains: housing demand has outpaced the pace of new supply where people most want or need to live. Population growth, migration, planning bottlenecks, high construction costs, and limited land in major metro areas all add pressure.

That is why Australian housing often feels as though it stays expensive even when affordability metrics flash bright red. Demand may wobble, but not enough to truly solve the imbalance. In other words, the market keeps saying, “Yes, this is painful,” and then raising prices anyway.

Price Trends: America Is Cooling; Australia Is Splitting

The U.S. housing market in 2026 looks like a market that is expensive but no longer overheating nationally. Prices are still high, yet national growth is modest. That creates a weird mood: homes are unaffordable enough to frustrate buyers, but not rising fast enough to feel thrilling for sellers. Everyone is mildly annoyed, which is actually a form of progress.

Australia’s market is more visibly split. Nationally, values remain very high, but city-level differences are doing a lot of the storytelling. Some markets are setting fresh highs, especially where relative affordability still exists and migration has boosted demand. Meanwhile, Sydney and Melbourne have shown softer patches compared with faster-moving capitals.

This divergence is important. In the U.S., people often talk about “the national market” with some caution because local conditions vary widely. In Australia, that caution is even more necessary. One city can look exhausted while another behaves as if price growth is an Olympic event.

Buying Culture: Negotiation vs. Auction Nerves

The U.S. buying process is usually more negotiated

In the U.S., most home purchases happen through listed prices, negotiated offers, inspections, contingencies, and a closing process that can feel like signing paperwork for a minor moon mission. Buyers often expect room for negotiation, due diligence, and financing protections.

That structure can be stressful, but it usually gives buyers more checkpoints. You can inspect the property, negotiate repairs, compare loans, and potentially walk away under certain conditions. It is not exactly relaxing, but it is at least organized chaos.

Australia leans more heavily on auctions in major markets

Australia has a stronger auction culture, especially in large cities. For many buyers, that creates a much more public and emotional transaction. Auctions can move quickly, encourage competition, and push buyers to make hard decisions in real time. There is less of the slow dance and more of a “please make your biggest financial commitment while your heart rate doubles” vibe.

This difference matters because market psychology changes when homes are sold in front of a crowd. In hot Australian markets, auctions can amplify urgency. In cooler periods, they can also expose weakness quickly. The theater is real. So is the blood pressure.

Government Policy and Tax Incentives

Neither country leaves housing entirely to market forces. Both use policy settings that shape who buys, who invests, and how housing wealth is treated.

U.S. policy tends to support long-term ownership

In the United States, tax rules still favor homeowners in important ways. Mortgage interest can be deductible for eligible taxpayers who itemize, and many homeowners can exclude a significant amount of capital gains when selling a primary residence. These features reinforce the idea of housing as a long-term wealth-building asset, not just shelter.

The U.S. system also benefits from the infrastructure built around fixed-rate lending, Fannie Mae, Freddie Mac, and standardized mortgage products. That does not make homes cheap, but it does make the ownership model more predictable once a buyer gets through the front door.

Australia gives investors a louder role

Australia’s tax system has long been shaped by features such as negative gearing and the capital gains tax discount for investors. These settings have helped keep property attractive as an investment vehicle, even when affordability for owner-occupiers has become a growing political and economic concern.

Australia also uses buyer-support programs such as the expanded 5% deposit scheme for eligible first-home buyers. These initiatives can help some households enter the market sooner, but critics often argue that demand-side support works best when paired with more actual homes. Giving more people a ticket to the race is nice. Building more seats would also help.

Which Market Is Tougher for First-Time Buyers?

There is no universal winner here. Each market is difficult in its own special, character-building way.

In the U.S., first-time buyers struggle with down payments, high monthly payments, insurance costs, and limited starter-home inventory. But there are many metro areas where affordability is improving, inventory is rising, and buyers have more options than they had during the pandemic surge.

In Australia, the hurdle often feels steeper because prices relative to income remain punishing in major cities, and supply pressure is intense. Even when rates stabilize, the entry price can still look brutal. That pushes many younger Australians toward smaller dwellings, outer suburbs, family financial support, or delayed ownership.

If the U.S. first-time buyer problem is “Can I carry this monthly payment?” the Australian version is often “Can I even get on the ladder before the ladder moves again?”

What Sellers and Investors Should Notice

For sellers, the U.S. now rewards realism. Homes that are well-priced and move-in ready can still do well, but overpricing is getting punished more often as inventory improves. The days of slapping on any number and waiting for bidding wars are less dependable in many markets.

Australian sellers, by contrast, may still benefit from supply scarcity in many locations, though outcomes depend heavily on city, neighborhood, and price bracket. Premium markets can behave very differently from more affordable segments. Broad national confidence can hide a lot of local weakness.

For investors, the U.S. may offer more geographic flexibility and better chances to compare markets based on cash flow, rents, taxes, and local inventory. Australia remains highly attractive to many property investors because of its long-term price history, tax settings, and supply imbalance, but entry costs are high and policy debate around housing has become more intense.

Real-World Experiences: What This Comparison Feels Like in Practice

Talk to a typical American buyer in 2026 and you often hear a story about math, patience, and timing. They may have found a home they like, but the monthly payment is what decides everything. A house can look reasonable on paper until the mortgage rate, property taxes, insurance, and maintenance stack up like uninvited dinner guests. Many U.S. buyers are not saying, “There are no homes.” They are saying, “There are homes, but not many that fit my payment.” That is a subtle but important difference.

Now talk to a typical Australian buyer and the tone often shifts. The complaint is less about finding a mortgage structure they can live with over 30 years and more about how fast prices can move, how fierce competition feels, and how hard it is to save enough to get in at all. Buyers often describe the market as if the finish line moves every time they get closer. They save, prices rise, and suddenly the deposit target has grown again. It can feel like trying to climb an escalator that politely refuses to stop.

Sellers in the U.S. are also having a different experience from a few years ago. Some still benefit from strong equity and limited neighborhood supply, but many are discovering that buyers are pickier. Listings sit longer. Price cuts happen more often. Cosmetic flaws that buyers ignored in the frenzy now matter again. A seller who expected a weekend bidding war may instead get one decent offer and a buyer asking for credits after inspection. It is not a bad market. It is just a much less flattering mirror.

Australian sellers, especially in tightly supplied locations, may still feel more leverage. Even when sentiment softens, scarcity can keep a floor under demand. But experiences vary a lot by city and segment. In some places, sellers still walk into auction day hoping for fireworks. In others, they are learning that buyers are cautious, finance-sensitive, and no longer impressed by “guide prices” that seem written in a fantasy novel.

Renters feel the contrast too. In both countries, high rents make saving for ownership harder. In the U.S., renters may still find markets where relocation can improve affordability. In Australia, many renters feel pinned by low vacancy, rising costs, and fewer obvious escape routes in major metros. That creates a stronger sense that the housing system is not merely expensive, but structurally crowded.

Perhaps the clearest experience-based difference is emotional. The U.S. market often feels like a puzzle with too many numbers. The Australian market often feels like a race with too few openings. Both are exhausting. They are just exhausting in different accents.

Conclusion

The U.S. housing market and the Australian housing market share the same top-level problem: affordability is strained, supply is too limited in key areas, and buyers are making life-changing decisions under financial pressure. But the deeper mechanics are not the same.

The U.S. market is shaped by long-term fixed mortgages, a fading lock-in effect, and a gradual return of inventory. Australia is shaped by stronger rate transmission, a tougher structural supply squeeze, investor-friendly tax settings, and a buying culture that often feels more competitive and compressed.

So which market is better? That depends on what you value. If you want financing stability after purchase, the U.S. has a major advantage. If you are measuring long-term scarcity and the way housing remains deeply embedded in wealth creation, Australia stands out. Either way, buyers in both countries are learning the same lesson: housing is never just about houses. It is about policy, credit, psychology, timing, and the occasional need to laugh so you do not scream.